•

Accounting

•

Automate Accounts Payable

•

Security

July 3, 2026

QuickBooks Desktop ACH Payments to Vendors: Which Is Right for Your Firm?

How QuickBooks Desktop ACH Payments to Vendors Actually Work

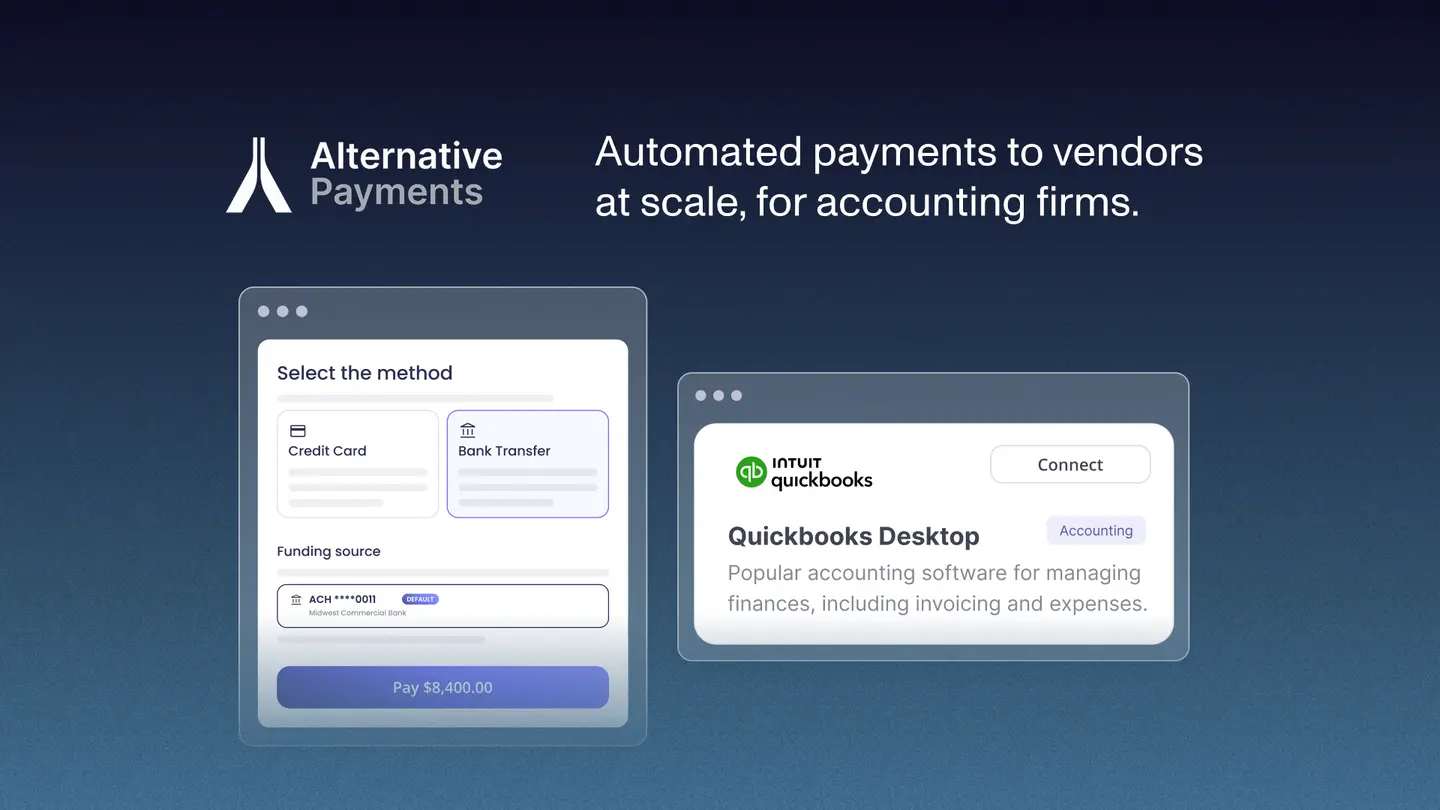

QuickBooks Desktop ACH payments to vendors work through Intuit's own payment network and require an active QuickBooks Payments subscription before any bank transfer can be initiated. The process is functional but involves several manual steps that accounting firms managing client books will encounter repeatedly.

The setup begins at the vendor record. Inside QuickBooks Desktop, you navigate to the vendor profile and enter the vendor's bank account number and routing number under the payment settings tab. QuickBooks stores this information and uses it to initiate transfers when bills are paid. Because this data lives inside the client's company file, each client entity requires its own vendor setup, there is no shared vendor directory across files.

To initiate a payment, you go to the Pay Bills window, select the outstanding bill, and choose the bank transfer option as the payment method. QuickBooks then queues the transfer through Intuit's ACH network. Depending on the subscription tier and the time of submission, processing begins on the next business day.

The approval process inside QuickBooks Desktop is limited. There is no built-in multi-step approval workflow for vendor payments. A user with pay bill permissions can initiate a transfer without a secondary review step. For accounting firms acting as the bookkeeper or controller on a client's account, that absence of an approval layer is worth flagging before setup begins.

According to Intuit QuickBooks Support documentation, ACH transfers through QuickBooks Payments typically settle within two to five business days, depending on bank processing times and submission cutoffs. Same-day ACH is not available through the native QuickBooks Desktop flow.

What Accounting Firms Need to Know Before Setting Up Vendor ACH in QuickBooks Desktop

Accounting firms managing vendor ACH in QuickBooks Desktop on behalf of clients face setup requirements that go beyond what a single-entity business user encounters. The compliance and permission considerations compound quickly across a multi-client practice. Before initiating a single transfer, four areas warrant deliberate attention.

1. Client authorization. Storing a vendor's bank account number inside a client's QuickBooks file means the firm is handling sensitive financial data on that vendor's behalf. Written authorization from the client confirming the firm is permitted to initiate payments from the client's account is a risk management baseline, not an optional step.

2. User permissions. QuickBooks Desktop assigns access roles at the company file level. The firm needs to confirm which staff members have pay bill access on each client file. In a CAS-model firm where multiple team members work across multiple client files, an unreviewed permission structure can result in payments being initiated without the right level of oversight.

3. Data security. Vendor bank account numbers stored inside QuickBooks Desktop company files are only as secure as the firm's file storage and access controls. If client files are stored on a local server or shared drive without encryption, that data carries the same exposure as any other file on that network. Firms managing 10, 20, or more client entities hold a significant volume of sensitive vendor banking data and that exposure warrants a deliberate policy on access, storage, and backup.

4. Multi-client complexity. Each client has its own vendor list, its own bill pay history, and its own QuickBooks file. None of that information is visible across clients simultaneously. A firm running vendor ACH for 30 clients is operating 30 separate payment workflows with no shared visibility, no centralized audit trail, and no consolidated view of what has been paid, what is pending, or what failed.

Each of these four points is manageable for a firm with a handful of clients. Across 20 or more, they compound into a workflow risk that is worth addressing before the first payment goes out.

The Hidden Costs and Delays of QuickBooks Desktop ACH for Vendor Payments

The costs of QuickBooks Desktop ACH payments to vendors are real, though not always visible in the moment a payment is initiated. Settlement times, per-transaction fees, limited status visibility, and manual re-entry across client files all add up across a practice.

Settlement time is the most immediate friction point. ACH transfers through Intuit Payments typically take two to five business days to clear, according to Intuit's published documentation. For a vendor expecting payment by a specific date, that window requires the firm to initiate the transfer several days in advance. If a bill is approved late or a file is not reviewed in time, the vendor receives payment late regardless of when the firm intended to pay.

Transaction fees apply to each ACH transfer processed through QuickBooks Payments. Intuit's published fee structure for QuickBooks Desktop ACH transactions charges a per-transaction fee on each bank transfer, separate from any monthly subscription cost. For a firm processing vendor payments across dozens of client accounts each month, those per-transaction fees accumulate across every bill paid for every client, making the true cost of the workflow higher than the subscription price suggests.

Real-time payment status visibility is not available through the native QuickBooks Desktop ACH flow. Once a transfer is initiated, the firm sees a queued status inside the Pay Bills history, but there is no live update when the transfer clears the vendor's bank. If a vendor calls to confirm receipt, the firm has to wait for the settlement window to close before confirming with confidence. That lag creates communication friction that a firm managing client relationships cannot easily absorb.

Manual re-entry is the compounding cost that scales with client volume. Each client company file in QuickBooks Desktop is a separate environment. A payment initiated for Client A does not inform the workflow for Client B. Vendor records, bill approvals, and payment histories have to be managed inside each file independently. For a firm handling vendor ACH across 20 or more clients, that means 20 separate bill pay workflows, 20 separate reconciliation processes, and 20 separate sets of vendor banking records to maintain and secure.

Where QuickBooks Desktop Falls Short for Multi-Client AP Workflows

QuickBooks Desktop falls short for multi-client AP workflows primarily because it was designed for a single business entity, not for a firm managing payments across many client companies simultaneously. The gaps that emerge at scale are structural, not fixable through add-ons.

The absence of a centralized payment dashboard is the most operationally significant gap. When an accounting firm manages vendor payments for 15, 30, or 50 clients, there is no view inside QuickBooks Desktop that shows all pending bills, all initiated ACH transfers, or all overdue payables across those clients at once. The firm's team has to open each client file individually to check payment status, review aging bills, or confirm that a scheduled transfer went through. That file-by-file workflow does not scale.

Batch vendor ACH payments across client files are not possible in QuickBooks Desktop. A firm cannot group vendor payments from multiple client accounts into a single approval and execution run. Each client's bills have to be paid from within that client's file, using that client's bank connection, on a separate login session. The time cost of that repetition is significant when multiplied across a full client roster on a monthly payment cycle.

Audit trail limitations create risk when clients or partners need payment verification. QuickBooks Desktop logs payment activity inside each company file, but there is no consolidated audit trail that a firm can produce across clients without exporting and compiling data from multiple files manually. If a client's lender, an external auditor, or a partner requests a payment history across a specific period, the firm assembles that report by hand. That process takes time the firm is not billing for and introduces the risk of a gap or error in the compiled record.

For accounting operations managers thinking about workflow efficiency and risk, the core problem is the same across all three gaps: QuickBooks Desktop treats each client company as a closed environment. Managing AP at the firm level requires a view that QuickBooks Desktop cannot provide without significant manual workarounds at every step.

QuickBooks Desktop vs. QuickBooks Online for Vendor ACH: What Is Actually Different

QuickBooks Desktop and QuickBooks Online differ meaningfully in how they handle vendor ACH payments, and the gap matters for accounting firms advising clients on whether to migrate or stay on Desktop.

QuickBooks Online offers automated bill pay through its native bill payment feature, which allows recurring vendor payments to be scheduled and processed without manual initiation each cycle. QuickBooks Desktop requires manual entry in the Pay Bills window each time a payment runs. For a firm managing vendors with predictable monthly charges, that difference in automation depth has a real impact on staff time.

Integration options are broader in QuickBooks Online. Because it is cloud-based and built on an open API, QuickBooks Online connects to a wider range of third-party AP automation platforms than Desktop. QuickBooks Desktop integrations exist but are more limited in scope and require more configuration to maintain. Firms evaluating third-party tools for vendor payment automation will generally find more options designed for QuickBooks Online than for Desktop.

Cloud access changes the workflow for multi-user environments. QuickBooks Online allows authorized users to access client files from any location without a server or VPN. QuickBooks Desktop requires either a local machine or a hosted environment to access company files remotely. For CAS firms with distributed teams or remote staff, that infrastructure requirement adds cost and complexity that QuickBooks Online eliminates.

Intuit has been reducing investment in QuickBooks Desktop over several years, and many firms running Desktop are being pushed toward Online as Intuit phases down Desktop support, discontinues older Desktop versions, and moves product development to its cloud platform. Firms advising clients who are still on Desktop should account for that trajectory when evaluating whether to invest in optimizing a Desktop-based AP workflow or migrate to Online and build from there.

The honest comparison for most CAS firms: QuickBooks Online handles vendor ACH with more automation and fewer integration constraints, but it is not purpose-built for multi-client AP management at the firm level. Both versions leave the same centralized dashboard gap that firms managing many client accounts need to fill with a third-party platform.

How Accounting Firms Automate QuickBooks Desktop ACH Payments to Vendors at Scale

Accounting firms automating vendor ACH payments beyond QuickBooks are using third-party B2B payment platforms that integrate with QuickBooks Desktop or Online and handle AP at the firm level, not just the entity level. This category of platform was built specifically for the multi-client, recurring-payment workflows that QuickBooks alone cannot manage.

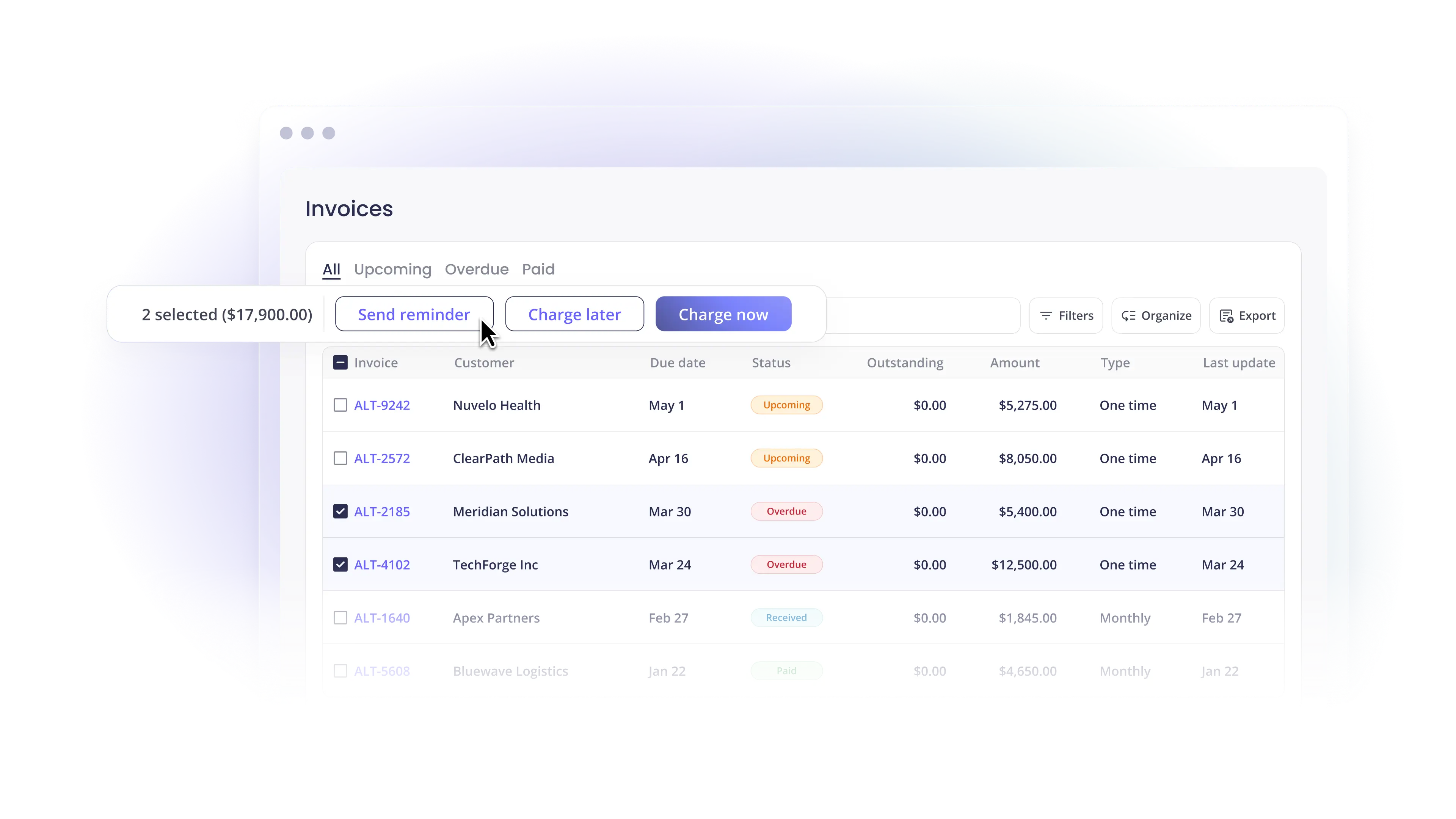

The defining feature of a purpose-built AP automation platform is a centralized multi-client dashboard. Instead of opening each client's QuickBooks file to review outstanding bills and initiate payments, the firm's team sees all clients, all pending payables, and all payment statuses in a single view. That consolidation is what makes vendor ACH workflows manageable at scale. A firm handling AP for 40 clients can review, approve, and initiate payments across all of them from one interface rather than 40 separate sessions.

Same-day ACH is available through platforms that connect to the ACH network directly rather than routing through Intuit's payment processing layer. For vendor payments that need to settle faster than the standard two-to-five-day window, same-day ACH closes the gap. According to NACHA (2024), same-day ACH volume grew significantly year over year as businesses moved time-sensitive payments off check and wire and onto the faster ACH rail.

Approval workflows are another feature the category provides that QuickBooks Desktop does not. A third-party platform can require a secondary reviewer to approve a vendor payment before it is initiated, which matters for accounting firms that need to maintain separation of duties on client funds. That approval log also becomes part of the audit trail, so payment verification requests from clients or partners can be answered with a structured record rather than a manually assembled export.

Remittance delivery is built into purpose-built platforms as well. When a vendor ACH payment is sent, the platform notifies the vendor with remittance detail: which invoice is being paid, the amount, and the expected settlement date. That communication reduces inbound vendor inquiries to the firm and to the client, which is a meaningful time savings across a full AP cycle.

Alternative Payments serves accounting and CAS firms running exactly this workflow. The platform integrates with QuickBooks and Xero, provides a multi-client AP view, supports ACH and card payments, and handles remittance delivery and reconciliation as part of the same flow. Unlike horizontal billing tools not built for accounting firm workflows, Alternative Payments is designed around the contract-driven, multi-entity billing model that CAS practices run on. For firms that have outgrown what QuickBooks Desktop can provide for vendor ACH at scale, it is a purpose-built next step.

Frequently Asked Questions

Q: Can you send ACH payments to vendors directly from QuickBooks Desktop?

A: Yes. QuickBooks Desktop supports ACH payments to vendors through its native Pay Bills workflow, but it requires an active QuickBooks Payments subscription. Vendor bank account and routing numbers must be entered manually in each vendor's profile within each client company file. There is no centralized vendor directory shared across multiple QuickBooks Desktop files.

Q: Does QuickBooks Desktop charge fees for ACH vendor payments?

A: Yes. Intuit charges a per-transaction fee for each ACH bank transfer processed through QuickBooks Payments, in addition to any monthly subscription costs. The exact fee depends on the QuickBooks Payments plan in place. For accounting firms processing vendor payments across multiple client accounts, those per-transaction fees accumulate across every bill paid for every client each month.

Q: What is the ACH payment processing time for vendor bills in QuickBooks Desktop?

A: ACH transfers initiated through QuickBooks Desktop typically settle within two to five business days, according to Intuit's published documentation. Same-day ACH is not available through the native QuickBooks Desktop flow. Firms managing vendor payments with time-sensitive due dates need to initiate transfers several business days in advance to avoid late payment.

Book a 20-minute demo and see how Alternative Payments cuts your DSO by 40%.

Simplify your customer payments, unlock instant cash flow

Keep reading

QuickBooks Desktop ACH Payments to Vendors: Which Is Right for Your Firm?

Payment Processing for Accounting Firms: Beyond Invoicing Software