•

IT Services

•

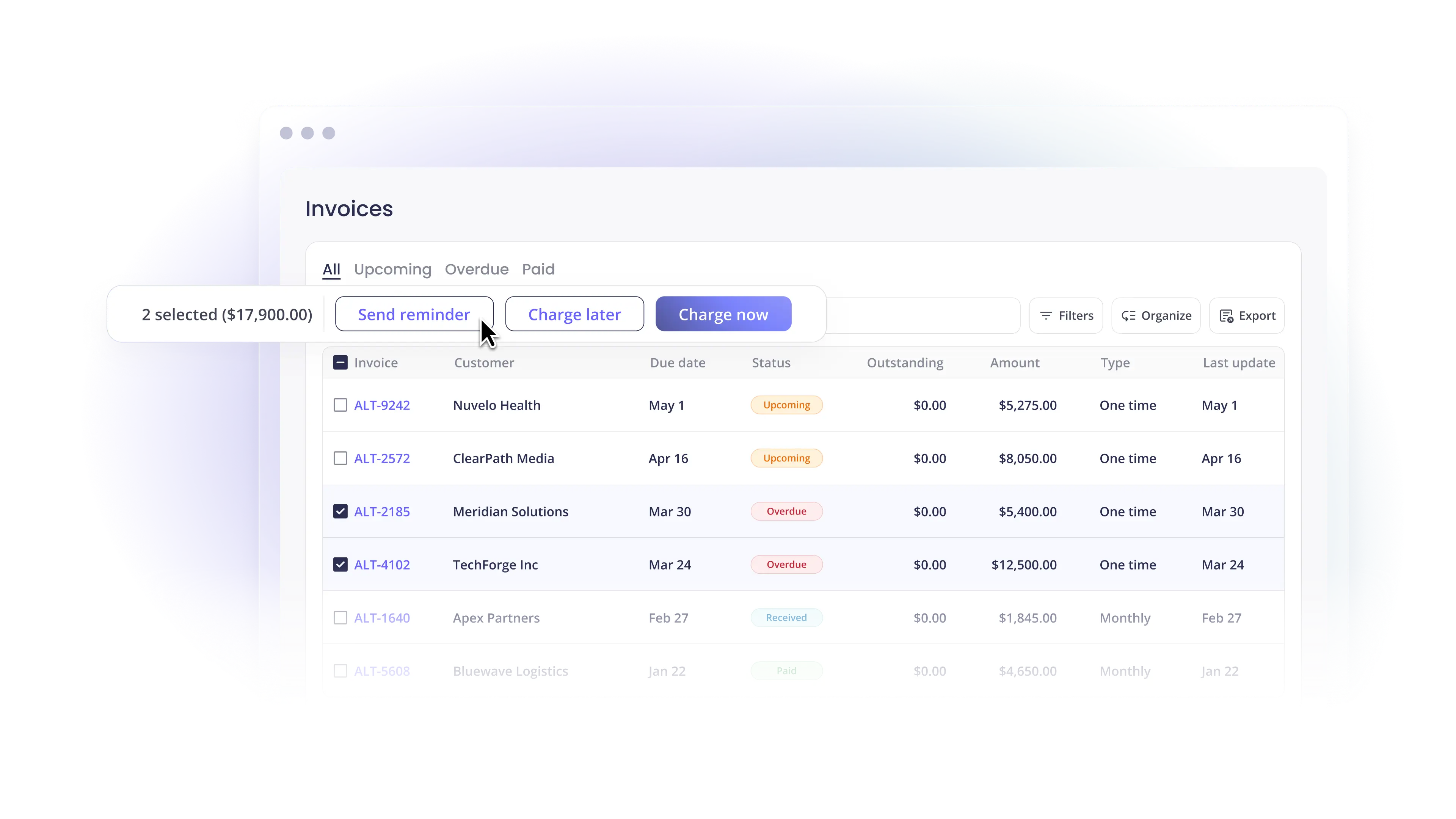

Automate Accounts Receivable

February 20, 2026

Why Micro Deposits Are the Ultimate Client Conversion Killer

Micro deposits were built for security.

But in modern B2B environments, they’ve become one of the most overlooked conversion killers in the client onboarding process.

For MSPs that rely on recurring ACH payments for managed services, this delay directly impacts onboarding momentum, service activation timelines, and the speed at which Monthly Recurring Revenue (MRR) begins.

You close the deal.

The agreement is signed.

The client is ready to move forward.

Then you tell them to wait two to three business days to confirm two small deposits in their bank account.

Momentum disappears.

The Problem with Traditional ACH Payment Verification

Traditional ACH payment verification relies on micro deposits to confirm that a client owns the bank account they entered.

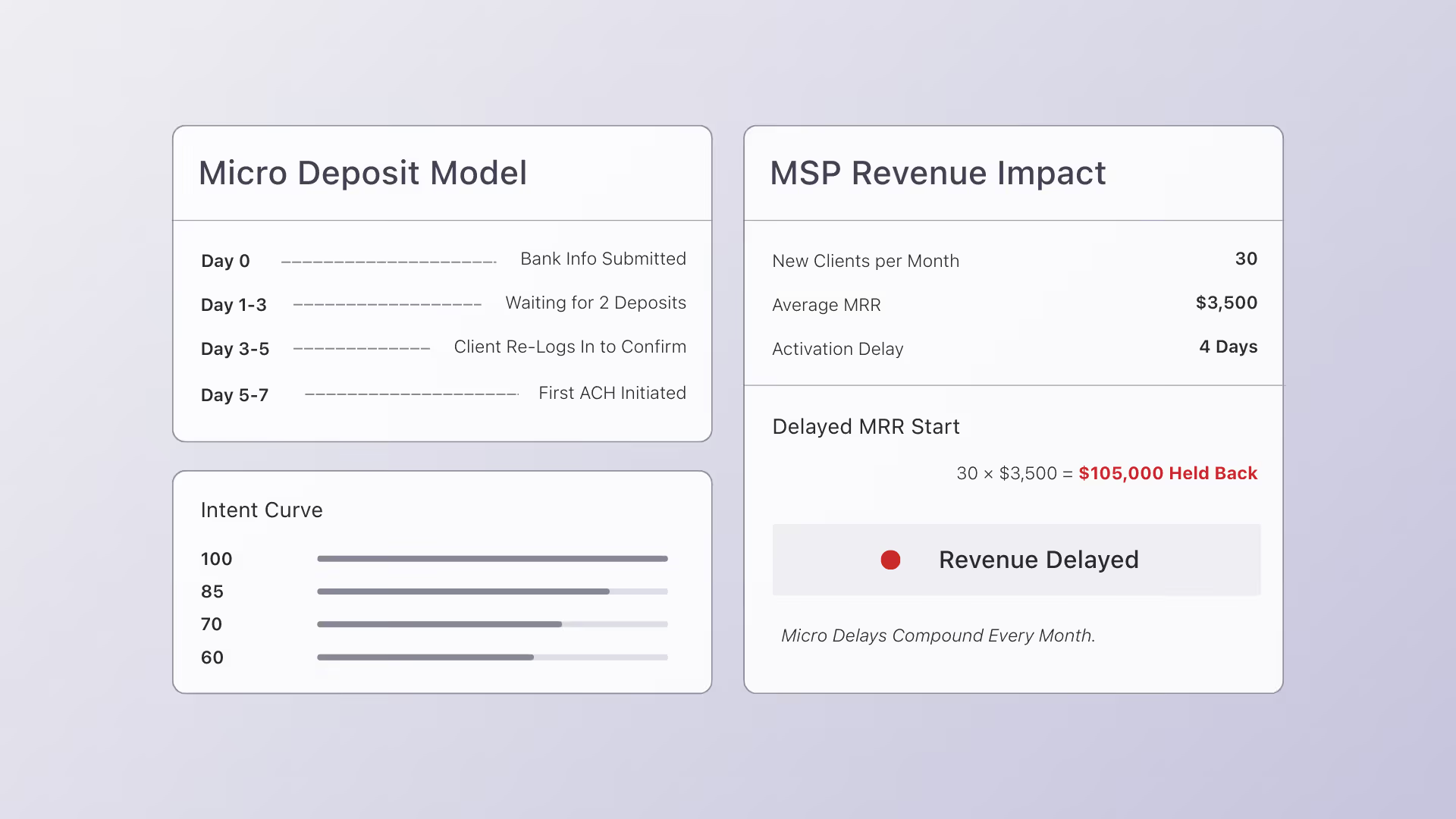

Here’s how it works:

- Two small deposits are sent to the client’s bank account

- The client waits one to three business days

- They log into their bank

- They return to your system and enter the exact deposit amounts

- If entered incorrectly, the process may reset

While this method verifies the account, it introduces unnecessary delay and friction into the payment experience.

And friction reduces completion rates.

How Micro Deposits Hurt Conversion and Cash Flow

Every additional step in onboarding increases the risk of drop-off. What may seem like a small procedural delay inside your organization can have significant downstream consequences across the client lifecycle.

When micro deposits are used for ACH payment verification, client activation slows immediately. Services that could begin the same day are pushed out by several business days. That delay often postpones the first invoice payment, which in turn delays revenue recognition.

What should be a smooth transition from signed agreement to active account becomes a waiting period defined by administrative follow-up.

In B2B environments, timing is critical. When clients say yes, that is the point of highest intent and alignment. They have secured internal approval. The budget is allocated. Stakeholders are engaged.

Introducing a multi-day verification delay creates space for distraction, shifting priorities, or stalled approvals. What felt urgent on Tuesday can easily become secondary by Friday.

For an MSP, that delay can mean postponed service onboarding, delayed RMM deployment, and a slower start to recurring billing. When onboarding momentum stalls, so does MRR.

The longer ACH payment verification takes, the more likely it is that payment is postponed — not because the client has changed their mind, but because momentum has weakened.

When this pattern repeats across dozens or hundreds of new clients, the financial impact compounds.

Delayed activations compress cash flow velocity, extend accounts receivable cycles, and quietly reduce working capital efficiency. For MSPs operating on recurring revenue models, even small onboarding delays compound into measurable MRR lag over time.

Micro deposits do not just slow down a single transaction. They slow down the movement of revenue through the entire organization.

The Hidden Operational Cost of Micro Deposits

The impact is not just external.

Micro deposits create internal administrative strain:

- Monitoring pending ACH verification requests

- Sending reminder emails

- Troubleshooting incorrect entries

- Restarting expired verification flows

Instead of accelerating onboarding, your team ends up managing avoidable workflows.

Micro deposits were built for security in a slower era of payments. They were not designed for the speed and scale expectations of modern recurring service businesses.

Real-Time Bank Verification: A Modern Alternative

Modern payment infrastructure no longer requires waiting days to verify a bank account.

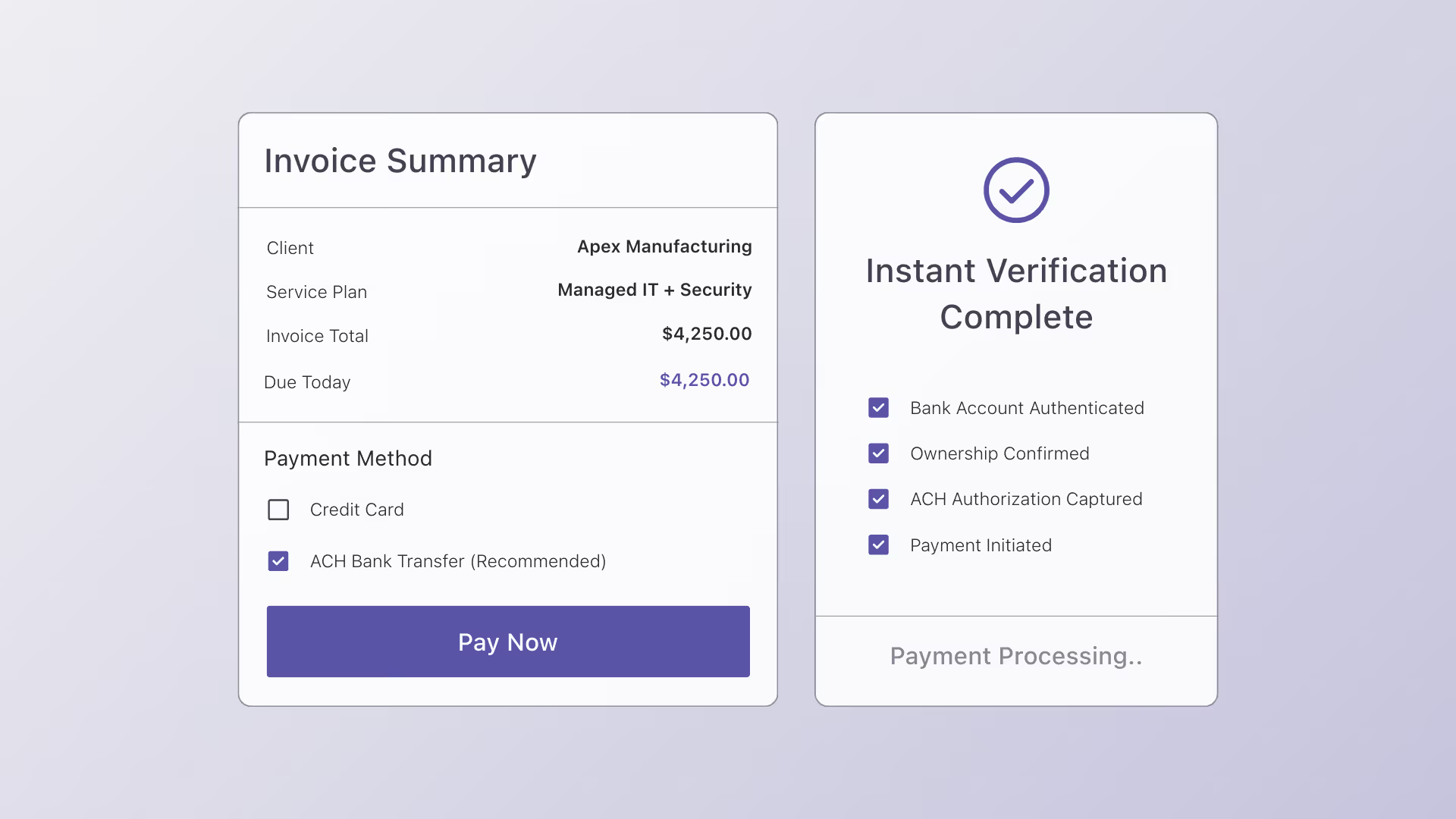

Today, real-time bank verification allows immediate authentication without micro-deposit delays.

Instead of sending small deposits, the process looks like this:

- The client selects their bank

- They securely log in through an encrypted connection

- The account is authenticated immediately

- The ACH payment can be initiated in the same session

No waiting period.

No manual deposit matching.

No follow-up reminders.

Verification and payment happen together.

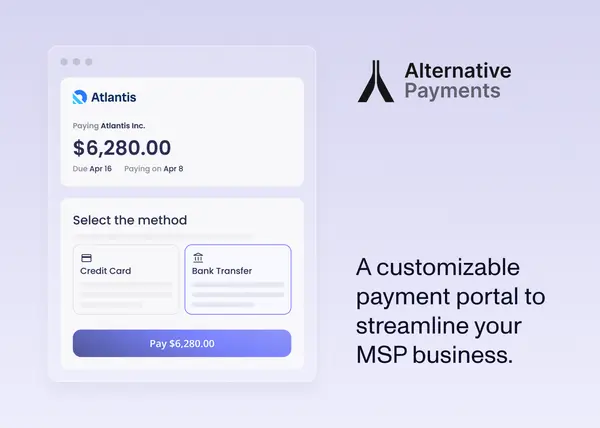

Turning ACH Payment Verification into a Seamless Experience

Alternative Payments replaces traditional verification methods with real-time bank verification built directly into the checkout experience.

When a client enters their payment information, they can securely authenticate their bank account immediately, eliminating the need for micro deposits altogether.

This modern ACH payment verification approach:

- Removes multi-day delays

- Protects conversion momentum

- Reduces onboarding friction

- Minimizes administrative overhead

- Accelerates time to first payment

Security standards remain intact, but the client experience becomes seamless.

Instead of asking clients to “check back in three days,” verification happens instantly, while engagement and intent are still high.

Why ACH Payment Verification Speed Matters More Than Ever

In competitive B2B industries, client experience is differentiated.

A slow, outdated ACH payment verification process signals legacy infrastructure.

A seamless real-time bank verification experience signals operational maturity.

The faster you remove barriers between agreement and payment, the faster revenue moves.

Micro deposits may seem small.

But in high-growth firms, small friction points create measurable revenue drag.

If your ACH payment verification process still relies on micro deposits, the real question is:

How much conversion momentum are you sacrificing because your system makes clients wait?

Simplify your customer payments, unlock instant cash flow

Keep reading

How a Customizable MSP Payment Portal Is Changing MSP Operations

Best Accounts Payable Software for Service Businesses (and When You Need AR Automation)