Most service businesses run their billing across three or more disconnected systems. The PSA generates invoices, a payment processor collects funds, and an accounting platform records deposits. Between those systems sits a gap, a manual, error-prone space where invoices get lost, payments go unmatched, and AR ages without anyone noticing until month-end closes.

That gap has a name: the reconciliation gap. And for MSPs, accounting firms, and other recurring revenue businesses, it costs real time, real cash, and real trust.

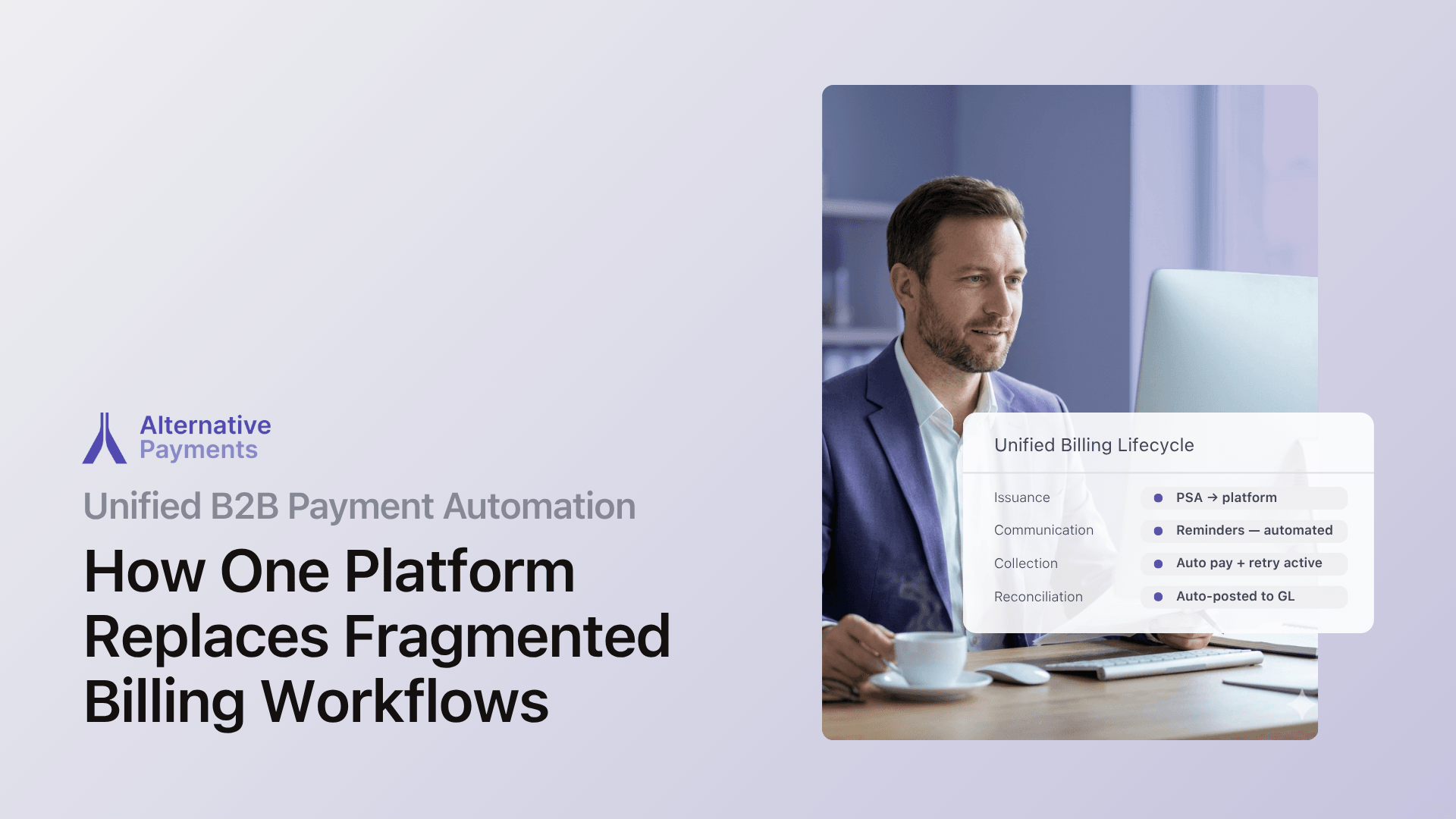

A unified B2B payment automation platform closes that gap by managing every stage of the billing lifecycle: issuance, communication, collection, reconciliation, and reporting, all in one connected workflow. Not by bolting tools together with middleware, but by building native connections between your PSA, your payment layer, and your accounting system.

This guide explains what makes a platform truly unified, which capabilities matter most, and how the right platform delivers measurable improvements in DSO, AR health, and operational efficiency.

What Makes a Platform “Unified” vs. “Integrated”

The terms get used interchangeably, but they describe different architectures, and those differences show up in your daily operations.

An integrated setup connects separate tools through APIs, middleware, or sync jobs. Your PSA talks to a payment gateway. The gateway talks to your accounting software. Data passes between them, sometimes on a schedule, sometimes with manual triggers. Each tool owns its piece of the process, and nobody owns the handoff.

A unified platform manages the full billing lifecycle natively. Invoices flow from the PSA into the payment layer automatically. Payment status updates push back to the PSA in real time. Settled transactions reconcile to your accounting system without manual matching. One system orchestrates the entire chain: issuance → communication → collection → reconciliation → reporting.

The practical difference matters most at scale. With integrated tools, every new client, every new agreement type, and every pricing change introduces a new potential failure point in the data handoff. With a unified platform, the workflow absorbs those changes because every stage shares the same data model.

Here’s what that looks like operationally:

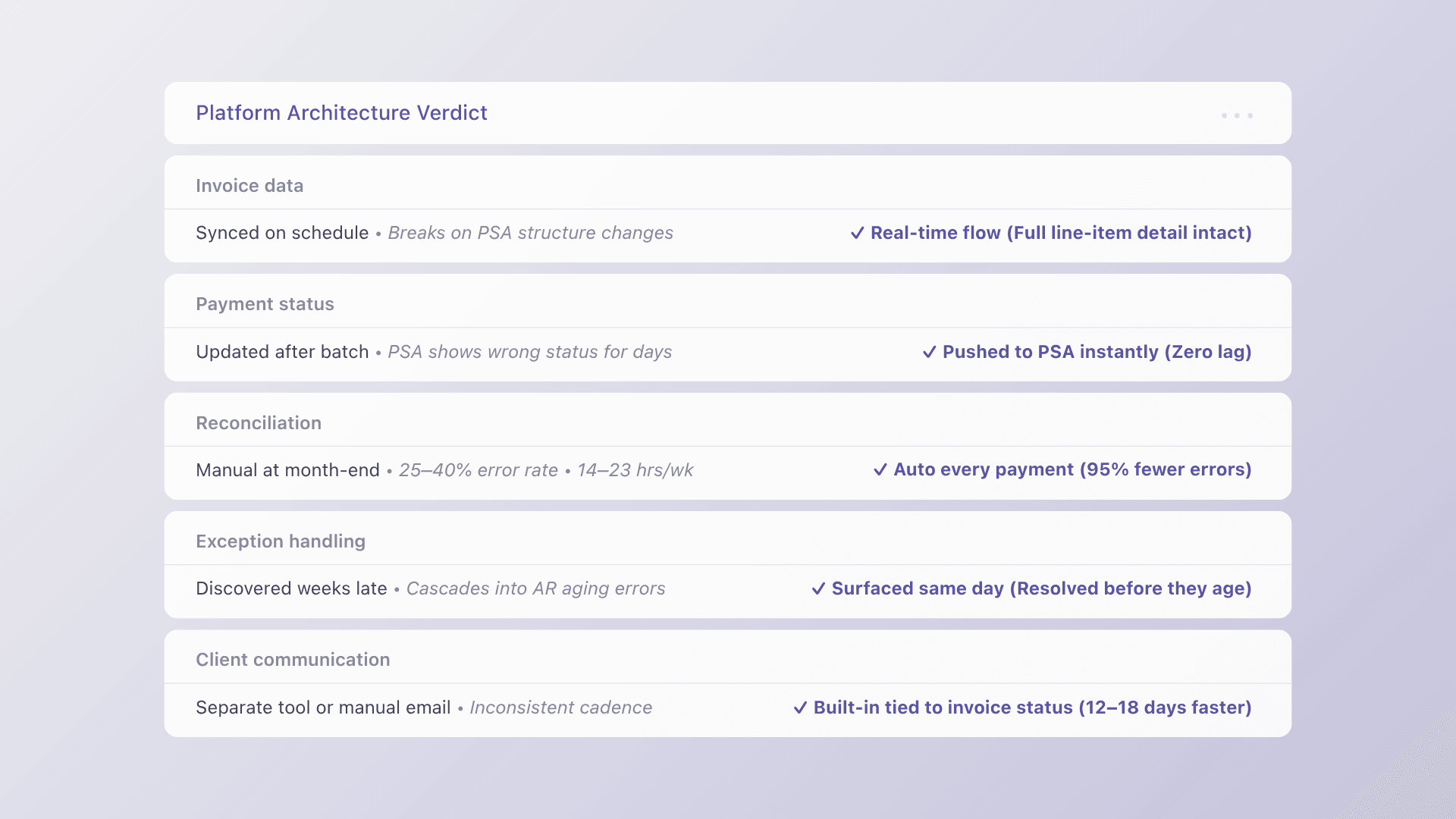

| Dimension | Integrated tools | Unified platform |

| Invoice data | Exported or synced on schedule | Flows automatically with full line-item detail |

| Payment status | Updated after batch sync | Pushed to PSA in real time |

| Reconciliation | Manual matching at month-end | Automatic, every payment maps to its invoice |

| Exception handling | Discovered days or weeks later | Surfaced immediately for resolution |

| Client communication | Separate email tool or manual follow-up | Built-in reminders tied to invoice status |

The Reconciliation Gap: Where Fragmented Workflows Break

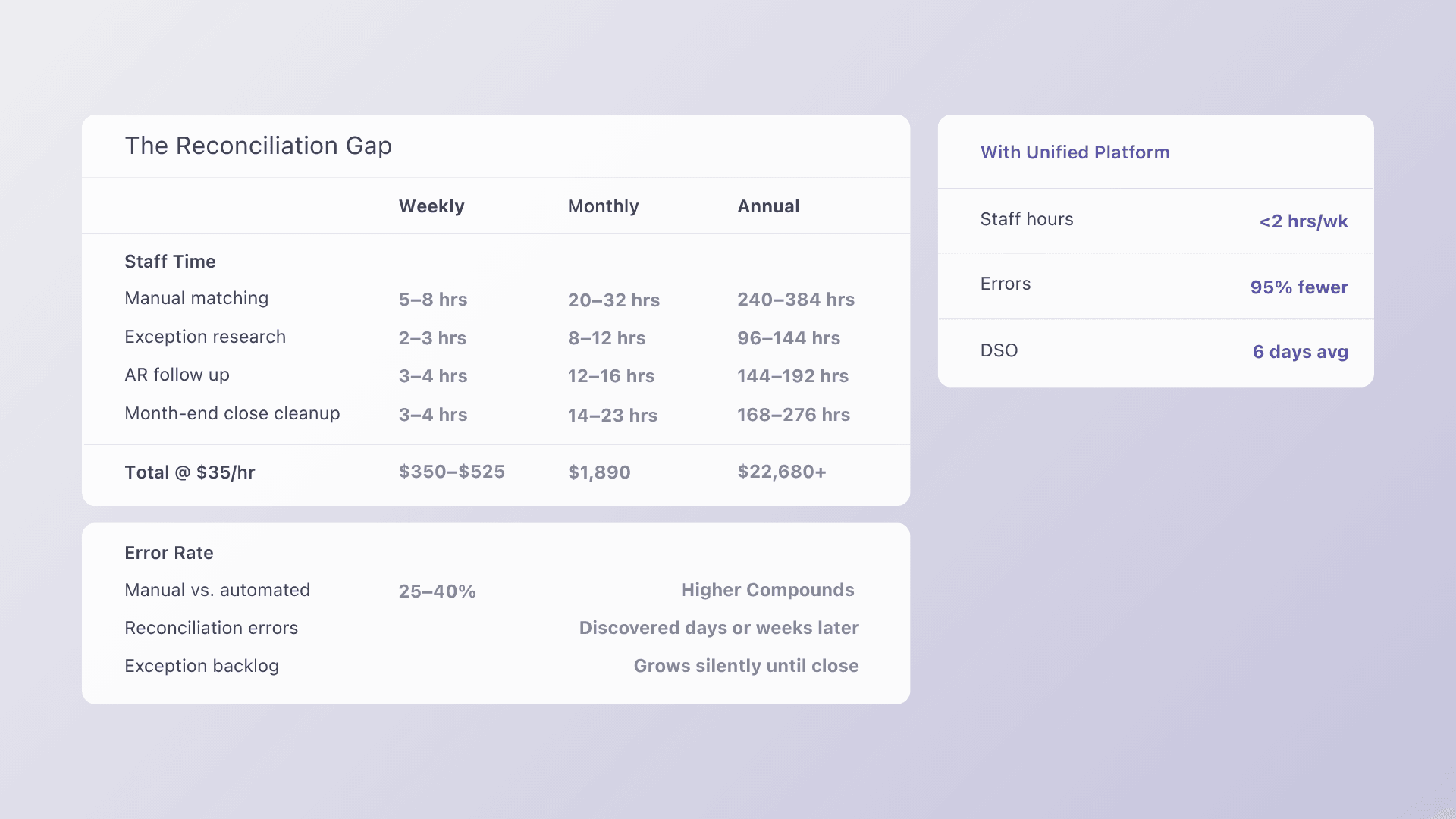

The reconciliation gap is the space between “invoice created in PSA” and “cash posted in accounting.” In a fragmented stack, this gap gets filled by people (your bookkeeper, your operations manager, or your finance lead) manually matching payments to invoices, chasing exceptions, and correcting mismatches before closing.

The cost is well documented. According to Paystand, finance teams at mid-sized companies spend 40–60% of their time on manual processes, including reconciling payments, chasing invoices, and entering data across disconnected systems. Accounting Seed reports that most finance teams spend 14 to 23 hours per week managing AR and AP functions alone.

The error rate compounds the time cost. According to ResolvePay’s analysis of reconciliation data, staff spend 5–8 hours per week on manual matching tasks, and manual processes carry a 25–40% higher error rate than automated alternatives.

For recurring revenue businesses, these problems compound monthly. A missed payment on one invoice creates a cascade: the aging report is wrong, the follow-up communication goes to the wrong client, and the exception sits unresolved until someone catches it. Meanwhile, DSO creeps upward. The industry benchmark for professional services sits at 30–60 days, according to CreditPulse’s 2025 analysis, and businesses running manual billing workflows typically land at the high end of that range.

Five Capabilities That Close the Gap

A unified platform doesn’t just collect payments. It manages the full lifecycle from PSA to GL. Here are the five capabilities that matter most for service businesses evaluating their options.

1. Native PSA integration

Native means bidirectional, real-time, and without middleware. Invoices created in your PSA (ConnectWise, Autotask, HaloPSA, or SuperOps) push directly to the payment platform with full line-item detail. Payment status, settlement data, and client responses push back automatically.

This matters because bolt-on integrations, the ones wired together through Zapier or generic APIs, typically import invoice totals without line-item detail, require manual mapping between PSA entities and accounting categories, and create reconciliation gaps that compound over months.

The right question isn’t “Does it integrate with my PSA?” It’s “Does it sync bidirectionally, in real time, with no middleware required?”

2. Automated reconciliation

Every payment should map to the specific invoice it covers and post to your accounting system automatically. No spreadsheets. No manual matching. No month-end scramble.

Automated reconciliation delivers measurable results. Finance teams using automated tools report a 95% reduction in reconciliation errors compared to manual methods, and month-end close processes shrink from days to hours.

For MSPs and service businesses, this also means your GL stays current. When a client pays by ACH on Tuesday, that payment hits the right invoice and posts to QuickBooks by Wednesday, not whenever someone gets around to the manual import.

3. Collections Assist and AR automation

Overdue invoices don’t manage themselves, and most finance teams can’t afford a dedicated collections function. Collections Assist solves this by embedding collections support directly inside the payment platform. You submit overdue invoices, and the system activates automated collections workflows without the extensive paperwork or separate vendor relationships that traditional collections agencies require.

This matters because the historical success rate for delinquent receivable recovery is approximately 40%, according to Alternative Payments, meaning businesses may recover only $0.40 for every delinquent dollar without structured intervention.

Broader AR automation adds another layer: automated reminders timed to invoice status, transparent client communication, and proactive strategies that prevent invoices from becoming overdue in the first place. CreditPulse’s data shows that automated reminder cadences outperform manual follow-up by 12–18 days on average.

4. White-label client portals

Client experience shapes payment behavior. A branded, frictionless checkout reduces time-to-pay and eliminates the confusion that comes with sending clients to a third-party processor that looks nothing like your business.

White-label checkouts present multiple payment methods (ACH, credit cards, and client-facing financing options), in a single, branded experience. Clients see your company name, your branding, and a clear path to pay. Behind the scenes, the platform maps their payment to the right invoice and triggers reconciliation automatically.

This is one area where purpose-built platforms diverge sharply from generic processors. A standard payment gateway processes a transaction. A unified platform processes a transaction and connects it to the client’s contract, the originating invoice in the PSA, and the correct GL entry in accounting.

5. Client-facing financing

Not every client can pay the full invoice immediately. Offering installment options, ACH, credit cards, and B2B buy now pay later through one checkout gives clients flexibility while protecting your cash flow.

The key is that financing options stay inside the platform. You get paid; the client gets terms. The invoice status, payment schedule, and reconciliation all happen automatically. No separate financing vendor, no manual tracking, no gaps in your AR data.

Measuring the Impact: What Changes When You Go Unified

Switching from fragmented tools to a unified platform produces measurable results across three dimensions.

Faster collections

According to Alternative Payments’ 2024 B2B Payment Trends Report, businesses using the platform reduce DSO to an average of 6 days, a 78% reduction compared to the industry average. For a $10 million revenue company, that reduction can yield a $597,260 cash flow benefit.

Fewer overdue invoices

Alternative Payments’ operational impact data shows that without the platform, 20.5% of invoices remain overdue. With it, that number drops to 6.7%. On-time and early payment rates increase from 37.5% to 61%.

Less manual work

42% of payments are now fully automated across businesses using AR automation tools, according to Alternative Payments’ proprietary data. That’s time returned to your team, time previously spent on manual matching, exception research, and follow-up emails.

Generic Processors vs. Purpose-Built Platforms

If your current processor treats invoices like ecommerce transactions, you’re leaving efficiency on the table. Here’s where purpose-built platforms differ:

- Contract awareness. Generic processors don’t understand PSA agreements, recurring billing cycles, or tiered pricing. Purpose-built platforms respect contract logic and map payments to the right agreement terms.

- Lifecycle management. Generic tools handle one stage: collection. Purpose-built platforms manage the full lifecycle, from issuance through reporting, so fixes address root causes, not symptoms.

- Accounting integration. A generic gateway deposits funds. A unified platform deposits funds and posts them to the correct GL entry in QuickBooks or your ERP, with the invoice reference intact.

- AR visibility. Generic processors show you transaction volume. Purpose-built platforms show you DSO, exception rates, on-time payment ratios, and aging, the metrics that actually drive decisions.

FAQ

What does “unified” mean in the context of B2B payment automation? A unified platform manages the entire billing lifecycle: issuance, communication, collection, reconciliation, and reporting, all in one connected workflow. Unlike integrated setups that pass data between separate tools, a unified platform shares a single data model across every stage, eliminating manual handoffs and reconciliation gaps.

How does PSA integration reduce manual reconciliation? Native, bidirectional PSA integration means invoices and payment status flow automatically between your PSA (ConnectWise, Autotask, HaloPSA, SuperOps) and the payment platform. Settled transactions reconcile to your accounting system without manual matching, so your GL stays accurate without spreadsheets or month-end scrambles. Learn more in our PSA integration guide.

What is Collections Assist? Collections Assist is Alternative Payments’ embedded collections solution. It lets service businesses submit overdue invoices directly within the platform, activating automated collections workflows without separate vendor contracts or extensive onboarding. It addresses the reality that delinquent receivables historically have only a ~40% recovery rate without structured intervention.

Can clients choose how they pay? Yes. A unified checkout supports ACH, credit cards, and client-facing financing options, including installments and B2B buy now pay later, in one branded experience. Clients pick their method; the platform handles reconciliation automatically.

Which businesses benefit most from unified payment automation? Service businesses in the U.S. and Canada with recurring revenue models, including MSPs, accounting firms, and telecom businesses, see the biggest gains. These companies rely on contract-driven billing, PSA workflows, and accounting integrations that generic processors weren’t designed to support.

Close the Reconciliation Gap in Your Billing Workflow

If your team spends hours matching payments to invoices, chasing overdue clients, or correcting GL mismatches, the problem isn’t effort, it’s architecture. A unified platform replaces that manual work with automated workflows that connect your PSA, your payment layer, and your accounting system.

Book a demo to see how Alternative Payments connects every stage of the billing lifecycle, from invoice to deposit, without the duct tape.