•

IT Services

•

Automate Accounts Receivable

November 18, 2025

The Real Cost Analysis of Accepting Different Types of MSP Payments

MSP Payments are no longer just about processing, they’re a margin strategy where payment method selection directly impacts profitability. ACH volumes and values continue to climb across U.S. B2B payments, while card fees remain structurally higher. Nacha reports that in Q3 2025, the ACH Network processed 8.8 billion payments worth $23.2 trillion a ~10% YoY increase in B2B usage, underscoring the shift to bank-to-bank rails for recurring, high-value transactions (nacha.org).

This guide compares ACH versus cards with current 2024–2025 data and translates those findings into an MSP-specific playbook: real fee math, cash-flow impact, decline risk, and the infrastructure you need to operationalize an ACH-first policy.

What card fees really cost in 2025

Card acceptance remains convenient, but expensive at scale. 2025 averages compiled by Helcim and summarized by The Motley Fool show typical processing of 1.8–2.6% + fixed fees for in-person and ~2.2–3.0% + fixed for online/keyed transactions—higher for premium cards and card-not-present flows (The Motley Fool).

Even after new legal and policy pressure, structural costs persist. A Nov 10 2025 Financial Times analysis of the Visa/Mastercard settlement noted that interchange would decline by only ~0.1 percentage point over five years—material but modest relative to baseline fee levels.

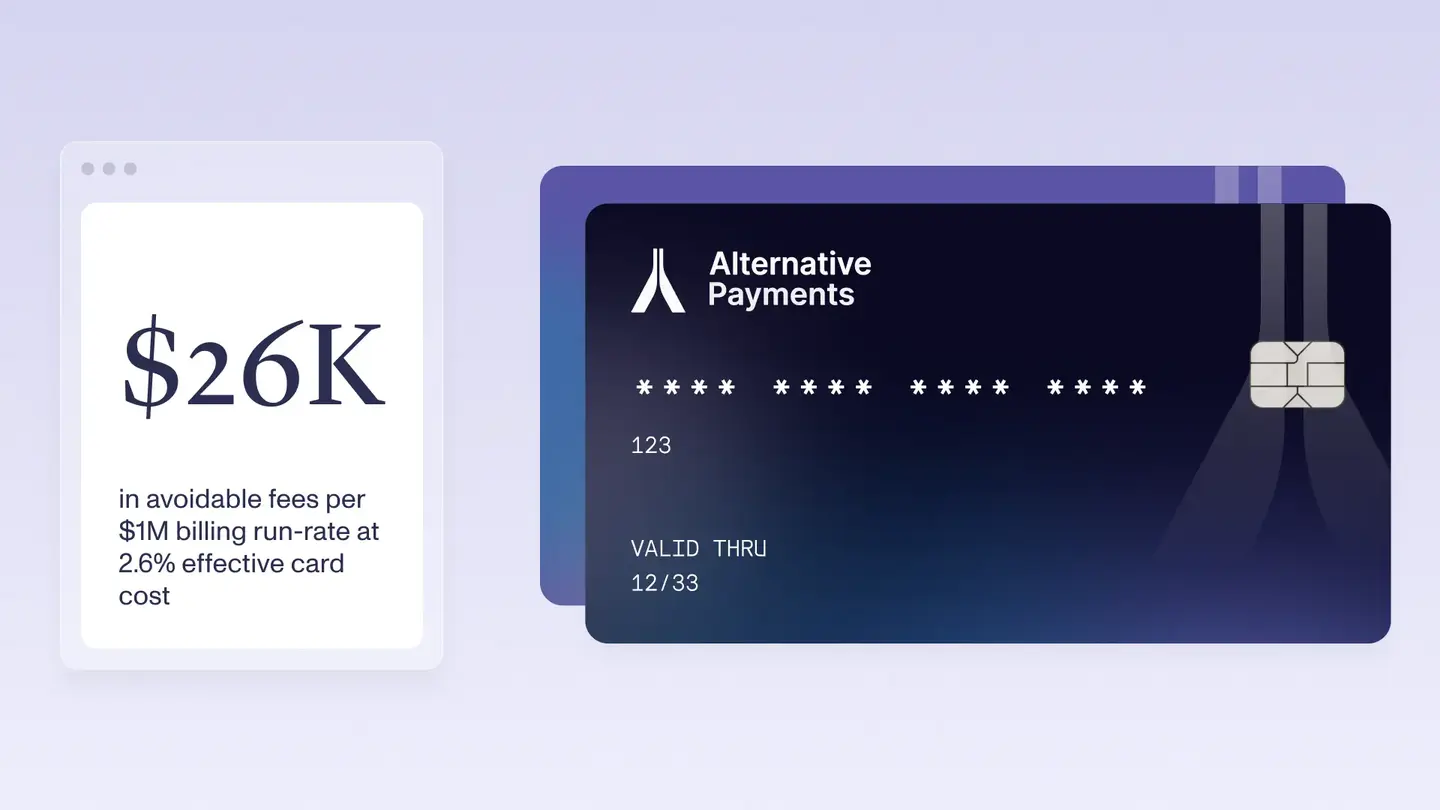

MSP takeaway: At a $1 million annual billing run-rate, a 2.6% effective card cost results in $26,000 in avoidable fees, before any gateway or chargeback adjustments. That level of leakage directly reduces EBITDA.

ACH in 2025: Usage, Speed, and Total Cost of Ownership

ACH growth continues. Nacha confirms strong 2025 momentum: Q1 +4.2% volume YoY, Same Day ACH +19.1% YoY and +24.8% value YoY, with B2B as a leading use case (mywespay.org). In March 2025, Nacha reported that 2024 ACH transactions exceeded 40 billion, cementing it as the backbone for large, recurring B2B flows (nacha.org).

Cost profile: ACH typically prices flat (cents) or low basis points, not card-like percentages. Multiple 2025 B2B studies place ACH at $0.20–$1.50 per payment or roughly 0.5–1.5% at the high end, while cards routinely run 2.6–3.5% + fixed (resolvepay.com).

MSP takeaway: For recurring invoices or project milestones, ACH converts a variable % drain into a predictable, and often negligible cost. Each payment routed through ACH preserves margin by avoiding the percentage-based fees charged by card networks.

Cash-flow Effects, DSO, Declines, and Involuntary Churn

Payment method choice determines both speed and certainty of cash. The Federal Reserve’s 2024 Business Payments Study found that U.S. businesses increasingly prefer electronic payments for reconciliation speed, remittance data quality, and working-capital control (FedPayments Improvement).

Card-on-file, while common, introduces recurring decline risk: expired cards, limit changes, and fraud flags. In subscription-style MSP billing, failed card payments remain the #1 driver of involuntary churn. Recurly’s 2025 retention benchmark confirms that automating decline management and offering alternative rails can recover up to 70% of otherwise lost renewals (Recurly Inc.).

MSP takeaway: ACH autopay avoids card-specific failure modes (expiry or reissue), improving renewal continuity and smoothing DSO volatility. Predictable cash flow becomes the result of thoughtful payment system design.

Compliance & policy, surcharging rules, caps, and legal nuance by state

If you continue to accept cards, know the rules. In most U.S. states, credit-card surcharging is allowed with disclosure requirements; Visa’s merchant guidelines detail these parameters. Independent 2025 legal updates compiled by Merchant Cost Consulting track each state’s signage, caps, and prohibitions for transparent policy design.

Be aware: even with permissions, network rules cap surcharges—Visa’s own limit ≈ 3%—and the recent interchange adjustments don’t materially change the economics (Merchant Cost Consulting 2025).

MSP takeaway: Transparent surcharging may indirectly influence more clients to choose ACH, but compliance should remain the primary focus. Ensure your disclosures, caps, and signage comply with both card-network and state regulations.

Pricing strategy: Pass the Fee, Discount for ACH, or Mix?

Pass-through: Recover card costs transparently

Pass-through pricing is the most direct and financially neutral model. Under this approach, the MSP charges the client the exact cost of paying by credit card, allowing them to choose the more cost-efficient payment method if they prefer. This preserves MSP margins without altering baseline pricing.

Observed Benefits

Clients who value their credit card rewards can keep them, and MSPs protect their margins. Those who want lower costs have a built-in incentive to switch to ACH. This turns the decision into a rational cost calculation rather than a negotiation.

Legal and compliance considerations:

As emphasized in Visa’s merchant surcharging guidelines and 2025 state-by-state updates from Merchant Cost Consulting, pass-through fees are permitted in most U.S. states but must follow:

- Clear disclosure

- Caps (typically 3% max, depending on network rules)

- Correct labeling (surcharge vs convenience fee)

- Uniform application across card brands

For MSPs, this means pass-through can be a safe and defensible option if implemented with transparent policies and consistent language. Many providers structure their portal so clients see the surcharge amount in real time before paying, reducing disputes and smoothing acceptance.

Psychology behind why pass-through works:

Behavioral pricing research shows that when the “true cost” of a method is surfaced at the moment of decision, up to 40% of users will switch to the lower-cost alternative. This is one reason why SaaS vendors widely use checkout-level fee visibility to shift users toward bank-powered rails.

When implemented transparently, pass-through models can help clients understand the real cost of each method.

Cash-discount / ACH incentive: Reward the cost-efficient behavior

Instead of charging more for cards, the ACH incentive flips the psychology: reward the behavior that costs less. In an ACH incentive model, your standard price assumes ACH, and credit card users pay the “non-discounted” amount. Clients see this not as a penalty but as a reward for choosing the method that helps both parties.

The Federal Reserve’s 2024 Business Payments Study provides strong support for this model. The study found that businesses increasingly favor payment methods that improve working-capital visibility, reduce reconciliation strain, and tighten cash-flow cycles. ACH is the clear leader across all three metrics.

Business Impact:

- It feels positive, not punitive

- Reduces objections

- Enables clearer financial forecasting

- Works well with autopay programs

- Allows the MSP to maintain a “clean base rate”

Quantifying the incentive:

Most MSPs use a 1%–2% ACH discount, which is still significantly cheaper than absorbing a 2.6%–3.5% card fee. At scale, this becomes a margin accelerator.

Example for a $12,000/yr client:

- Card cost at 2.9% = $348 lost annually

- ACH discount at 1.0% = $120

- Net savings for the MSP vs card: $228

When multiplied across 40–100 clients, this becomes tens of thousands annually.

And because incentives anchor behavior, once clients choose ACH for the discount, they rarely switch back. Once clients opt into ACH, they tend to maintain it as their default payment method.

Hybrid model: ACH default, cards for edge cases

The hybrid model is increasingly common in 2025 because it blends client flexibility with strategic margin control. In this structure:

- ACH is the default or pre-selected payment method

- Cards remain available, but are opt-in

- Incentives or surcharges may still apply

This model works well for MSPs with mixed client profiles:

- Large B2B customers who prefer ACH

- Smaller or international clients who favor cards

- Clients who occasionally need on-demand or emergency services

Why the hybrid works:

Because default choice architecture is one of the strongest forces in behavioral economics. The famous “opt-in vs opt-out” research shows people stick with the pre-selected choice over 80% of the time.

When ACH is the default in the billing portal, clients naturally follow it unless they have a strong reason not to. You shift the entire payment mix without forcing it.

Understanding the break-even math

As ticket size rises, percentage-based card fees erode margin exponentially. ACH’s flat or low-bps cost structure wins every time. This is why resolvepay.com’s 2025 B2B payment comparison shows ACH outperforming cards at every invoice size above $300.

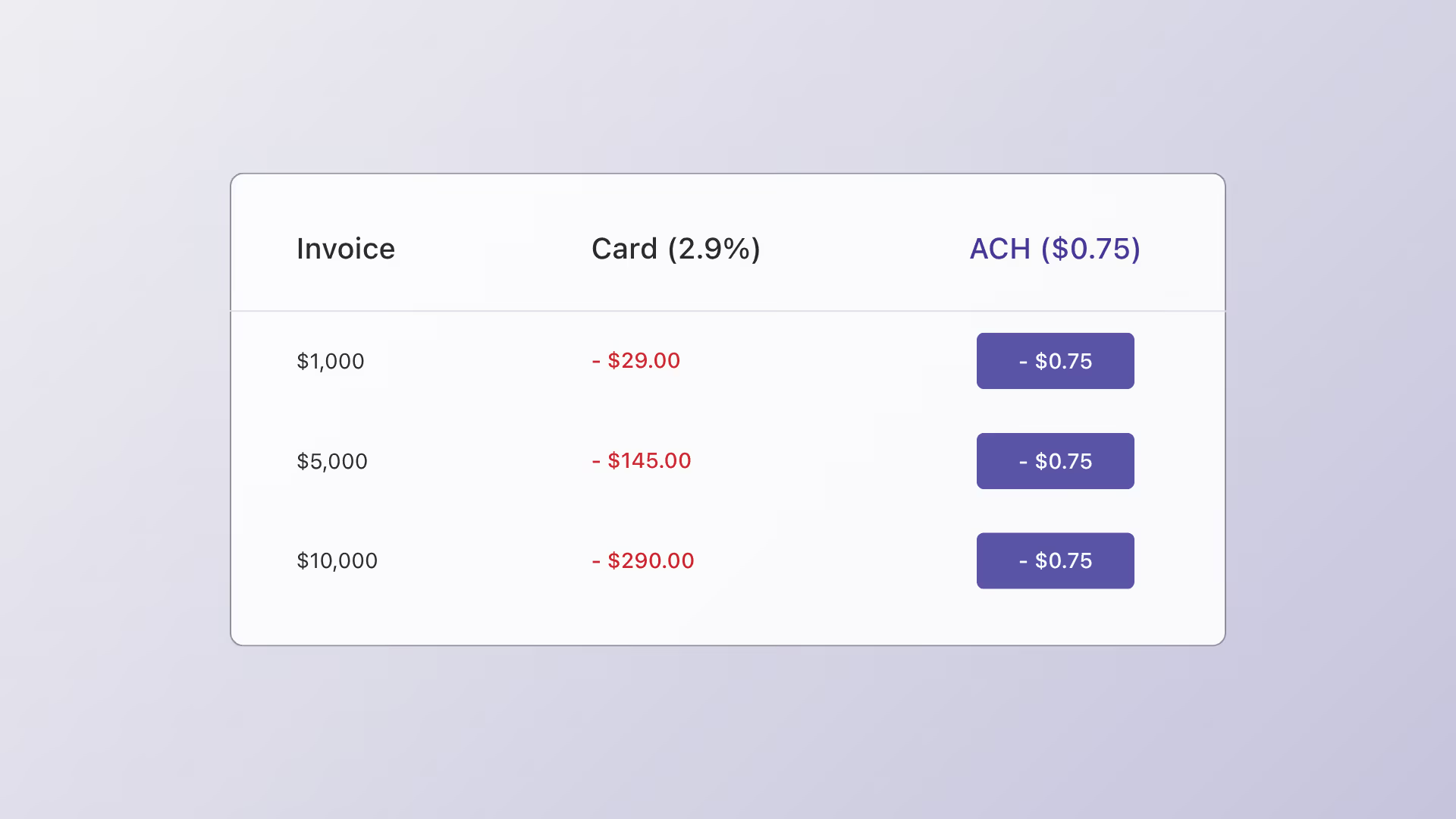

Break-even example:

- $5,000 invoice

- Card at 2.9% = $145 cost

- ACH at $0.75 = $0.75

- ACH saves: $144.25

Scaling this across recurring monthly agreements compounds savings dramatically.

Which model should MSPs choose?

Here’s the strategic observation based on 2025 data trends:

- Small-ticket MSPs (<$500 invoices): Hybrid, with subtle incentives

- Mid-size MSPs ($500–$5k invoices): ACH incentive model

- Enterprise-focused MSPs: Strong preference for pass-through or ACH-only

- MSPs in high-fee verticals (healthcare, finance): ACH preferred for compliance + predictability

- MSPs scaling for acquisition: ACH-first recommended for valuation uplift

Why acquisition? Because payment reliability directly affects recurring revenue stability—a core metric in valuations.

Whether you choose pass-through, ACH incentive, or hybrid, the goal is the same:

Move clients toward cheaper, lower-risk payment rails without damaging trust.

With the right pricing strategy and portal design, MSPs can reshape payment behavior quietly and permanently—unlocking stronger margins, smoother cash flow, and a more predictable revenue engine.

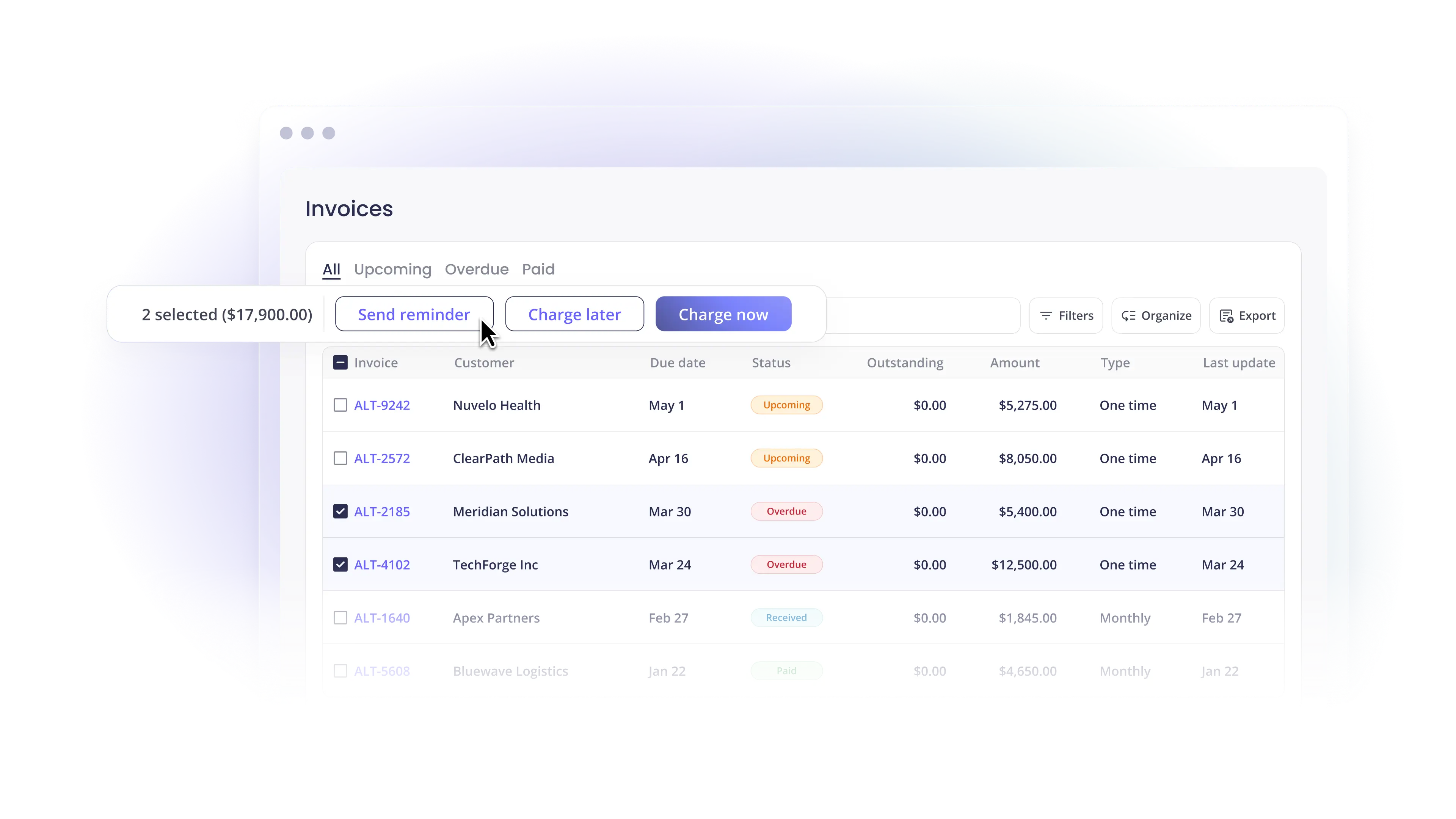

Infrastructure Checklist to Support Advanced Payment Methods

To turn these insights into results:

- Payment rails: Enable ACH—including Same Day ACH for time-sensitive transactions. 2025 throughput proves its readiness (mywespay.org).

- Policy engine: Autopay defaults, intelligent retries, and secure bank-account tokenization.

- System links: Integrate PSA ↔ billing ↔ accounting to automate reconciliation.

- Analytics: Monitor DSO trends, success vs decline rates, surcharge recovery, and ACH adoption.

MSP Benchmark: Providers See Stronger Retention When More Clients Shift to ACH

- Show the math: Quantify each client’s annual savings from ACH versus cards.

- Make ACH the default: Pre-select ACH in your payment portal; keep cards as opt-in.

- Offer a gentle incentive: A 1–2% ACH discount often beats credit-card reward economics at B2B invoice sizes.

- Reduce friction: Bank-account tokenization plus a one-time e-mandate makes setup seamless.

- Promote reliability: Reference Recurly’s 2025 findings—ACH minimizes failed payments and accidental cancellations (Recurly Inc.).

With transparent communication and a data-driven narrative, clients perceive ACH not as a limitation but as an operational upgrade.

A Data-Driven Payment Mix for Long-Term Health

MSP Payments strategy is a lever for margin, not just a checkout preference. 2025 data show ACH adoption accelerating while card costs remain structurally higher, even after incremental fee concessions.

The winning mix is straightforward:

- ACH as the default,

- Cards as an exception,

- Transparent surcharge or discount policies, and

- Infrastructure that automates reconciliation and tracks performance.

In practice, MSPs can start by benchmarking their current payment mix, piloting an ACH-first policy, and tracking DSO improvements over one quarter.

Simplify your customer payments, unlock instant cash flow

Keep reading

How a Customizable MSP Payment Portal Is Changing MSP Operations

Best Accounts Payable Software for Service Businesses (and When You Need AR Automation)