Imagine being able to afford a small business loan that will change the capabilities and profitability of your company. That’s what Alternative is doing with its integrated solution for the changing landscape of interest, approval rates, and ultimately alternative online payment methods.

Baxter Lanius, CEO, and Founder at Alternative walks us through the company’s goals and niche market.

Join us as we discuss:

• How Alternative is creating a unique buying experience for buy now, pay later

• Macro trends in the debt capital market

• Why embedded finance is the payment of the future

Podcast Transcript

Intro: You’re listening to payments innovation, a podcast dedicated to helping business leaders navigate today’s global digital economy. Looking to learn about the latest innovations within fintech and payments, you’ve come to the right place. Let’s get into the show.

Brady: Welcome to another episode of the Payments Innovation podcast. This is your host, Brady Burkett. And today, I’m thrilled to have on the show, Baxter Lanius, CEO and founder of Alternative. Alternative is a B2B buy now, pay later that lets your clients pay over time. And I want to let Baxter introduce himself and the company. Baxter, welcome to the show.

Baxter: Awesome, Brady. Thanks so much for having me.

Brady: So, we’re gonna talk all about buy now, pay later and B2B payments today. But first for our audience, can you introduce yourself, your background and a little bit behind the origin story of Alternative?

Baxter: Yeah, of course, Brady. So, I’m the CEO and founder of Alternative as Brady mentioned. We’re a B2B buy now, pay later solution to empower customers to pay overtime to ultimately drive revenue. I have tremendous amount of experience in the fintech space. I started my career really on the investing side, working for a fund called Victory Park Capital, which was one of the first institutional accredited investors in fintech. And during that time, I sat on the boards of a number of early stage fintech companies, both seed, Series A, Series B companies, and really understood the nuts and bolts of building a lending business, both on the consumer side as well as the business side. And at that time, it was really fintech 1.0. Many firms were not necessarily doing much underwriting, it was really all about customer acquisition, and hanging in the proverbial online shingle, to acquire customers at a cheaper rate than what a brick-and-mortar bank or brick-and-mortar lending business could do. But it’s a really, really interesting experience between 2014 and 2017.

I then actually left Victory Park and I joined Apollo Global, which is a 600 plus billion-dollar private equity business where I invested in technology companies and learned more about kind of the broader technology ecosystem, which, as I started to dig into, realized was just kind of continuing to accelerate and shift. And it was specifically shifting within data integrations and API’s and the proliferation of the cloud. And companies for the first time, could really underwrite and really kind of get a pulse on the underlying fundamentals of businesses through these online channels and online technologies, leveraging APIs, and leveraging a number of these data integrations. And that’s when I really – it all clicked and I wanted to start Alternative because, my goal all along was, how do you create a better underwriting engine and a better Risk Assessment Engine. And that was the insight and that was the thesis that we really built Alternative on. And I’ve since grown into B2B payments and lending, to really better underwrite businesses and provide access to capital, and more capital at a much more accelerated rate.

Brady: And we’re going to talk all about really the emerging or the converging trends, that the Alternative sits in the middle of here in the fintech space today. But first, can you explain a little bit about how the product works?

Baxter: Yeah, of course. So, our product is all about driving revenue growth, as I mentioned. And as any listener knows, there are gazillion ways to drive revenue growth. One of the key ways that businesses in the later stages use is the ability to offer flexible payment plans and flexible payment solutions to their end customers. Now, for a lot of businesses, this doesn’t exist because they want to maximize cash up front. And what we’ve put together and what we’ve assembled, is a product that really aligns interest between the vendors and the customers and allows us to sit in the middle and allows your end customer to pay overtime, over six installments or twelve installments or three installments, and still allows you to get paid up front. And when you think about the power that this has, it really has a tremendous ability to unlock value in all sorts of different ways.

You know, if you have customers within your funnel that you haven’t been reacting to the latest product feature, you can leverage a pay overtime solution to pry them from that position in the funnel and get them to activate and get them to motivate to make a decision. If you’re trying to upsell and cross sell a customer on a new solution that may be more expensive, you can simultaneously offer them the ability to pay overtime. If you have a customer who’s about to churn, and you’ve identified them, because they’re not using your product or solution as frequently as other customers, you can use a pay overtime solution to retain that customer. And this tool is really a sales enablement tool. And it’s really, how do you align interests as best as you can, with your end customer, who oftentimes is a little bit more price conscious, is a little bit more price sensitive, and wants to maximize their dollars out the door.

Brady: Yeah. And I think you just used a phrase that I like, which is aligned interests or aligned incentives. And you’re speaking to the massive benefits here of driving revenue for the vendor or the supplier here in this scenario in the B2B transaction. And then obviously, the capital stands to benefit the buyer by giving them access to new features, or potentially entirely new SaaS contracts or new products that they can add to their business from day one, and pay overtime. So, can you talk a little bit about how you’re building this? It really feels like a three-way transaction where you’re providing capital, but it’s benefiting both the buyer and the seller. And it’s kind of like a win, win, win. But can you talk a little bit more about that, specifically within the B2B context?

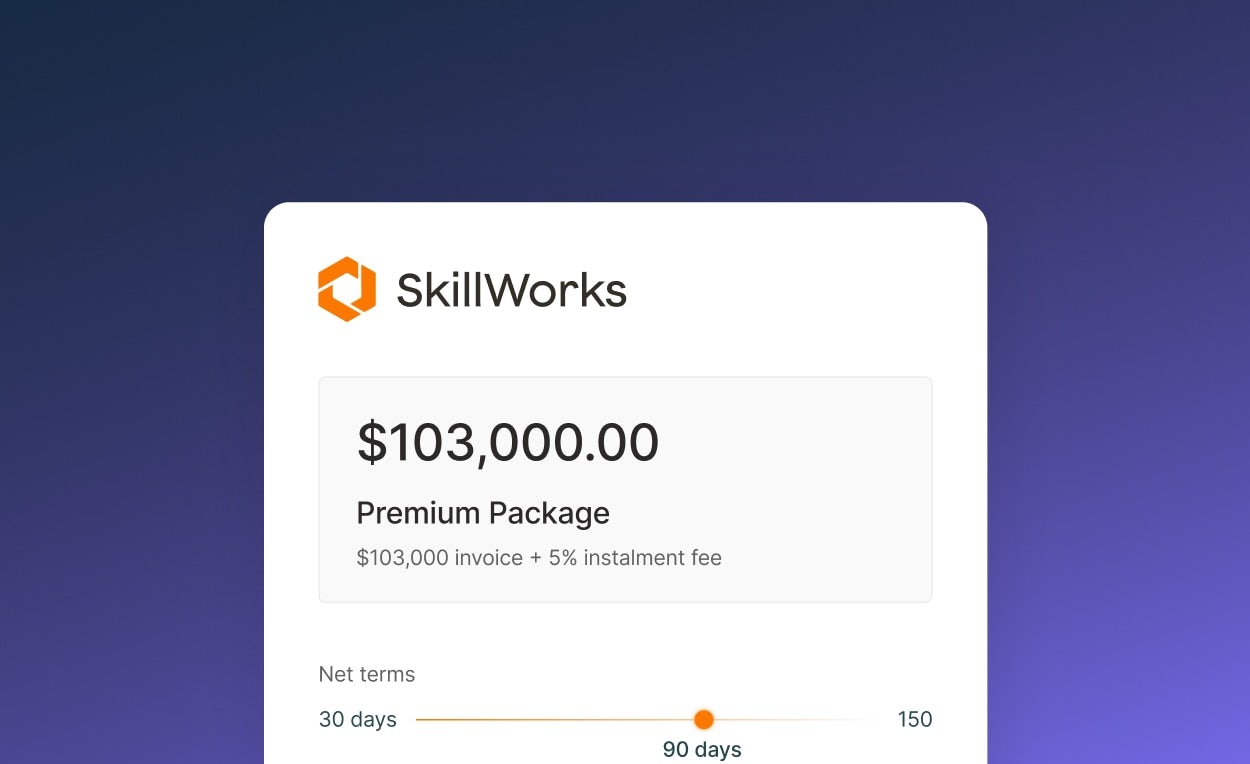

Baxter: Yeah, totally. So, let’s just walk you through a very specific example of how this functions and how this works. So, if you have a $50,000 transaction, and our default duration is about six months, or six installments. Our average duration is about four. But let’s say, again, you have a $50,000 purchase price, and you’re trying to convince your end customer to make that purchase. Now, with Alternative, you can set them up to a six-installment payment plan, requiring them to pay $8300 or $8,333 a month for six months. On day two, we would pay our vendor or our partner, we would take a 5% discount. So, we would pay them $47,500 on day two. So, they’re able to actually close on that transaction on day two, not even net 30 or net, net net 60. And then we would collect over six installments from the end customer.

Now, if you think about the broader risk that we’re taking. And to your point, Brady, in terms of it being kind of a multi-pronged relationship, we’re evaluating our partners on their ability to carry out the service, or, if it’s a software platform to execute on the contract for their software. In the event that they don’t execute, right, we’ve now fronted them the payment, and we’re trying to collect from the end customer and the end customer is upset, because, the service is, it’s not to a specific threshold. And so that’s super important to us. And we really focus on both the quality of product that all of our partners are offering, but then also their financial capacity and their financial fortitude, in terms of how much capital do they have in the bank, because that’s the first real risk. And then those are our real partners who use this for their end customers. But at the same time, we’re offering terms to the end customer, allowing them to pay over time for this solution. So, we also need to ensure that the end customer, we’re taking on the right risk within that end customer. And so, it creates this three-way relationship, where it’s clearly a win-win from our partner and the vendor and the supplier’s perspective, as well as the end customer. But we are evaluating risk across this ecosystem and across the system to ensure that the end customer can make those six payments in this example, and that we can recover the $50,000, or in this case $47,000, we would keep $2,500 from $50,000 total investment here.

Brady: Yeah, and I think this also is probably a nice segue. I’m sure a lot of our listeners are kind of tuned into what’s going on in the consumer buy now pay later market and it is a bit more of an established product. There’s a number of top players at this point, like Klarna and Sezzle and Affirm. And I think it’d be interesting to explore the differences here between B2B buy now pay later and consumer buy now pay later. I think, I’d be curious to hear your thoughts, but right off, off the bat, it seems to me that you don’t have some frivolous purchases that regulators would scrutinize like they do with consumer lending to go by fast fashion and things. And actually, the value of credit being provided to buyers. I just heard a quote listening to an interview with Elon Musk, where if he hadn’t paid his suppliers on time at Tesla, back when they were just getting started, he’d be out of business, right?

So, there is kind of this like, very objective difference in value of what credit can mean to a consumer versus a business. And maybe you can talk a little bit more about that. But also, we’re talking about the difference between a B2B payments channel and a consumer to merchant payments channel. And in my perspective, this might be an assumption, a consumer to merchant payment channel is pretty well developed, right? Either you use a debit card, or you use Klarna. But those are pretty, pretty workable solutions, not too many gaps there. In the B2B world, I think B2B payments, as many folks in fintech know is not a solved problem. There’s a lot of moving parts, there’s a lot of different elements to think about. So, maybe just in that lens of comparing to what our listeners probably understand a bit better at this point in the market. Can you talk about how B2B buy now pay later is fundamentally different than consumer?

Baxter: Yeah, totally. And there’s a lot to unpack there, Brady, between buy now pay later and B2B and consumer, as well as just the kind of broader B2B payments ecosystem. Ultimately, we work with our partners who are mostly business critical suppliers and vendors, and they’re offering very high value, high ROI type spend. And for us, the equation is all about how do you align your ROI in terms of dollars out the door to dollars in the door. So, let’s say that that $50,000 basket of goods or software that you’re purchasing is a high ROI spend. We’ve now broken that payment down into about $8300 a month for six months, and in month 2, 3, 4, 5, 6, you can now use that software to bring in revenue and to drive value for your business. So, that inherently is a very different purchase and then the consumer buy now pay later which is really all about consumption. Right?

I mean, Affirm and Peloton, that partnership was one of the preeminent partnerships within buy now pay later which partially drove Peloton’s success and drove a lot of the publicity around buy now pay later. Sure, you could classify it as a health and wellness purchase, but it’s all about consumption. And in the B2B space and to your point on Elon Musk, it’s really about managing cash flow. And it’s really about balancing that ROI. So, as we see it, we are allowing our partners to sell more to a broader end customer base that can now balance more of the volatility around cash flow. And that’s super, super important and doesn’t exist as much in the consumer space. The other piece, which is very different in B2B payments is, there’s really no online terminal as you experience it in the consumer world.

So, you don’t go to a specific website and check out and buy a Peloton as you receive an invoice via email or you receive a phone call saying that you owe $10,000. And that’s where our solution is fundamentally different than every single other B2B buy now pay later solution. Alternative solution runs complementary and we partner and we work with QuickBooks, Salesforce Quote-to-Cash, Zero, all these other accounting and invoicing solutions to provide you another offer and another solution to embed buy now pay later within that invoicing solution. So, we partner with these businesses, we work in parallel to these businesses to ultimately create more easy checkout experiences and fundamental payment transactions for those end customers. So, we’re actually not only providing this pay overtime solution. We’re also providing a much more succinct checkout experience, so that your invoices and so that your bills, can and will get paid over time because to your point Brady, the B2B payments ecosystem, I mean, I kind of like I laugh to myself, but it’s just it’s so antiquated and there are really not that many options to check out.

Brady: Yeah, and so, I think the B2B – I might come back and ask you more about your partnerships there with the actual financial software that the businesses are using. But with B2B, you don’t have that reliability, like an online merchant might, where if the debit card fails, you don’t have to ship them the goods, right? Like there’s so much more ambiguity in timing and delivery and payment receipt, where the contract signs and your teams start working on an implementation, just use a software use case, but the payment terms aren’t for seven days or 30 days. And then you have to reconcile that check in the mail. And it’s kind of a nightmare. The other thing that, I’m sure folks in accounts receivable departments in businesses across the country can relate to is, looking at simply like, like nonpayment and churn risk. And that could be either at the time of implementation or post going live, and it’s a monthly billing cycle, and clients just stop mailing that check. So, can you talk a little bit about, you were talking about Alternative’s impact to top of funnel sales. But when it comes to live client, what is that impact that you’ve seen? Or can you just talk about a few of those things that Alternative brings to the table for clients who have already signed the contract? And now they might just need a clear path for payment over the lifecycle of that relationship?

Baxter: Yeah, totally. And let’s go over the kind of the specific challenges that you mentioned, because I think that those are kind of the preeminent challenges within B2B. I mean, you mentioned ambiguity in terms of timing and delivery of payments, payment terms being delayed, the challenges in terms of reconciling different payments, or non-payments and churn. Alternative ultimately helps with all of it, right, because we set up a payment plan for the end customer, and we pay our partner and our vendor on day two. The payment plan is very well described and summarized within Alternative’s platform. You are due on May 18, $8,333. On June 18, you owe another $8,333. And so, it’s very, very clear. And we have a very transparent payment system to ensure the transparency on that side. Additionally, on the vendor side, you’re paid on day two, and we automatically reconcile your payments through our platform.

So, once the $47,500 payment hits your bank account, the status is updated in your dashboard. And both sides have complete clarity to the funds flow, which is hugely important to get comfortable with all these challenges. I think the one of the more fundamental issues is around nonpayment, bad debt expense and collections. And Alternative also helps tremendously with that, because we’ve set up the end customer on a very specific payment plan to ensure that, if nonpayment is a thing, we are communicating with that customer and we sit in in the middle as an intermediary. And so, we work with, typically on the selling side and on the sales cycle, we work with the head of sales, CEOs of businesses. Once we’re in the house, we typically work with the accounts receivable department. And, we work with the fundamental people who are sending out these invoices and using Alternative as an Alternative, no pun intended to get more deals done and to ensure nonpayment.

We have an ad tech company as one of our partners. And as everybody knows, in the ad tech space, once you collect or once you are paid, then you can begin the ad spend or the ad campaign. Now, for the specific customer and for all ad tech companies that work with us, we provide that insight to show them that they’ve received payment. It’s in the bank, and they don’t need to constantly refresh their Silicon Valley Bank account to see if that wire has hit. Once the status is updated to complete, they can immediately begin the ad campaign. And it’s seamless as opposed to refreshing, refreshing, refreshing your bank account and never knowing when that payment is coming in. And then a payment comes in for $8,500 and then you need to manually reconcile it. So, our solution really sits in between, and can be leveraged and utilized in a multitude of different ways. But we create transparency around timing of payments and payment terms. We create transparency around nonpayment and churn risk, as you mentioned, and it’s a huge, huge win-win for big problems in the B2B ecosystem.

Brady: Zooming out a little bit, you did mention partnerships with, I wasn’t sure, if you’re exclusively speaking to accounts receivable or both accounts receivable and accounts payable platforms. I can see an avenue for both. We talk a lot and to be honest, everybody in FinTech talks a lot about embedded finance. And, there are some interesting opportunities there. And I’m curious if you have thoughts on, how you see that evolving over time where what, to take QuickBooks, for example, like they might have started out purely as a software platform, but they’re gonna look for ways to bring more intensive financial services within their platform. I guess Question number one is, is Alternative there yet in exploring those types of relationships? And then either way, just curious if you have comments on that, as an executive and kind of what you see the future with those relationships with your partnerships there today?

Baxter: Yeah, no, it’s a fantastic question. And mid last year was kind of the high of this whole embedded finance theme. And I think a lot of these software companies will embed finance into their platforms in many different ways, whether it’s lending, or whether it’s accounts receivable, or AP, or whatever it is, or whether it’s stock brokerage accounts. There’s something really interesting about lending. And it’s very interesting, and the time today, given the macro and economic background, and a lot of people are scared to be a lender.

They don’t want to take on a bunch of balance sheet risks. They don’t want to have a balance sheet. They’d much rather be a software company. There’s the kind of old valuation metrics of, lending businesses should trade for book value. So, book value for lending businesses. If you have a $50 million book of loans, you should be worth $50 million. And if you trade at a slight premium of 1.25 times book, then, you’ll trade at a slight premium to your loan book. And that will actually I think provide a little bit of a barrier around getting into lending, because of that just kind of overall macro perspective. So, what was mid last year this like massive trend of embedded lending, may actually slow down. That said, there are a ton of companies that offer lending solutions that are embedded, and QuickBooks is actually one of them, right?

I mean, you have QuickBooks Capital, you have Square Capital. I’m sure a lot of entrepreneurs and CEOs receive emails from a multitude of different people offering them different lending solutions. However, distribution is obviously a differentiator in the market, but you’re going to need to differentiate and you’re going to need to come up with a much better underwriting solution to broader distribute your capital. And I think that that’s something that all embedded finance companies cannot necessarily do and cannot necessarily do easily. The way in which we’ve partnered with invoicing solutions really on the accounts receivable side is, we provide all of our partners with a white label link solution. So, for Currency Cloud, as an example, it would be currencycloud.financing.link, and that link, in turn is embedded within every single invoice that Currency Cloud sends out.

So, it’s actually a very simple, differentiated, unique approach to embedded finance, where if you want to check out via pay over time, you can immediately just click this Currency Cloud link, and pay for this invoice over time, as opposed to spending, four to eight months working with one of the embedded finance teams on how do you really embed this and integrate this appropriately, in a seamless manner. You can get started with Alternative in minutes. And that’s I think one of the challenges within embedded anything, right is, you don’t necessarily know what the return on investment of this initiative will be. And you really have to kind of take a leap of faith that the company that’s embedding with you can execute appropriately and drive that kind of value. So, I think the theme is definitely here to stay. It may slow down, especially on the capital intensity side where if you’re embedding with solutions that require a big balance sheet, but it just it allows companies to build faster, to expand their product feature set, and ultimately deliver a better solution to their end customers.

Brady: Yeah, a really interesting perspective there, Baxter. Thanks. Another macro trend that we’re seeing. For folks listening, we’re recording here, middle end of May 2022. And I want to get your thoughts on some of the macro trends in the capital markets. You sit at an interesting intersection here providing buy now pay later for businesses. And we talked a lot about cash flow today, and you hear how important it is now to watch your cash flow, because it could potentially become more difficult to raise equity capital moving forward with some of these deals, not coming through that founders were expecting. So, that’s like side one of the equation. And then side two, to be honest, I know much less about but that’s the debt capital market. And I’m not sure what’s going on there with expectations around rates, but ultimately, in the lending business, you do need to keep an eye on debt capital. So, can you just talk about both what the buyers, the sellers are seeing in terms of their own cash flow? What Alternative can bring to the table there, given today’s environment? And then also, if you have thoughts or comments on kind of the general macro environment about Alternative’s access to debt capital, and what you expect there moving forward?

Baxter: Yeah, definitely. So, I think we’re in a really, really interesting point in time, especially for a business like Alternative because ultimately, providing your end customers the ability to pay over time for your solutions is a huge win-win, and should especially be an even bigger win in this type of environment because every end customer is more focused on cashflow, and more focused on the ability to properly track and project their cash burn. So, if they can now pay for something that was $50,000, in $8,300 installments, they’re probably much more likely to make that purchase and move forward with that decision. So, I do think that, Alternative is a platform that will continue to see a lot of success in this environment, as people are very cashflow concerned and cautious. And I would advise every company to adopt a solution, like Alternative to better align interests with your end customers and make sure that you can get those deals done.

In terms of the broader macroeconomic and debt capital market side, you’ve already seen spreads widen on the consumer side, and we’ve already seen defaults start to tick up on the consumer side, which obviously is really a leading indicator for kind of more distress to come. And that will cause yields to rise. So, if you were raising capital, let’s say you are raising $50 million to lend out and previously, you were able to raise that capital at 2% or 3%, which is kind of where the securitization market was on the consumer side, you’re now raising it at 4% or 5%. And the challenge there is that, your cost base stays constant unless you obviously make cuts. And so that just directly eats into your profitability as a lending business. Right. So, if you were generating a 10% profit margin, and your cost of capital was 3%, for every 100 bps, you lose a little bit more on the profit margin side.

On the business side where we specifically focus and then B2B, we haven’t seen that much challenge in terms of raising capital and in terms of expanding our platform. Now, I’m sure that will come and so, we’re focused on expanding our balance sheet to ensure we have capital to fund. I think, the bigger question and the bigger concern and it’s really in line with what you’re seeing on the consumer side is, what do the loan books of these B2B lenders look like? And what are the underlying loans and what are the underlying companies that are contained in these loan tapes? And that’s something that I think people will take a magnifying glass to and ensure that they’re making the right underwriting decisions because there’s inherently a conflict of interest here, right?

The underlying lender is typically generating much more return associated with the equity value, and the value of his or her platform. The lender who’s providing the capital is holding the bag on their loan book. And so all of these online lenders and fintech companies are actually incentivized to open the floodgates and do a bunch of poor deals. And so, I think you will also see in the B2B space, some of lenders who will get exposed from taking on too much risk on the underlying business. But I haven’t seen that yet. And we’re definitely not there yet. But as the macroeconomic environment worsens, there will definitely be some holes in some of these portfolios.

Brady: Gotcha. Well, I really appreciate your perspective on that, Baxter. And thanks for sharing your thoughts. As we look to wrap up the conversation today, I’m curious if you can give us, you kind of gave us some forward-looking thoughts on the macro environment, but maybe about Alternative and B2B buy now pay later as a whole. You’ve explained the obvious value here for both the buyer and seller, and only how that value will grow if trends continue. But I’m just curious, where do you see the direction of the company going? Or, more generally, where the B2B buy now pay later market will go here?

Baxter: Yeah, I mean, I think it will continue to escalate. And in the US, there are not that many players that are currently competing in this space. And it’s a very clear value add and value prop from both sides of the equation. And there’s no reason why companies should not use buy now pay later, and the ability to pay overtime and installment plans to ultimately get access to capital, right? If you are a series A or you’re a small business, and you don’t qualify for a $250,000 loan, but you’re able to pay overtime for your $50,000 oven, or you’re able to pay overtime for your $30,000 whatever it may be, it’s a new way to ultimately get capital into the hands of small businesses who need capital and need incremental runway to survive. And that’s the same trend line that ultimately drove buy now pay later in the consumer market to so much success.

I think the key question in the B2B space is that, I think you’ll need more than just buy now pay later, or just lending to be super successful in the B2B space because it is a much more competitive, larger market. And I think you’re seeing a lot of innovation from all sides of B2B payments. So, I think that there’s a lower probability that you see Klarna, or Affirm equivalents in the B2B buy now pay later space. And you’ll see a lot of these B2B buy now pay later companies, of which there are only a handful today and most of them are based in Europe really, really expand into something much broader and much greater to help the accounts receivable team, to help the head of sales, to help the payment infrastructure for those specific businesses. And there’s going to be a lot of innovation in that space because, receiving PDF invoices or email invoices just can’t go on for much longer. Obviously, all these things have a much longer tail to them. But if I receive another PDF invoice, I mean, come on, guys, we need to do something here.

Brady: Yeah, well, good to know that at least you’re out there, taking a stab at solving this and really appreciate the time today, Baxter. It’s been great to learn about Alternative. Where can folks find out more about the product suite and get in touch with you?

Baxter: Yeah, definitely. So, our website’s alternative.co, you can find me on LinkedIn and Twitter at Baxter Lanius. My email is baxter@alternative.co, would love to chat with folks.

I think that we’re in a really, really interesting time in the buy now pay later space within B2B as well as the macro environment. And we’d love to hear from you all and thanks so much for your time, Brady. That’s been awesome.

Brady: Yeah, absolutely. Thanks.

Moderator: You’ve been listening to the Payments Innovation podcast. To ensure that you never miss an episode, subscribe now in iTunes or your favorite podcast player. Thanks for listening. Until next time.