•

IT Services

•

Automate Accounts Receivable

•

Small Businesses

•

Security

May 23, 2025

How to Encourage Clients to Pay via ACH (and Save on Fees)

A Fee Here, a Fee There… and Then It Hurts

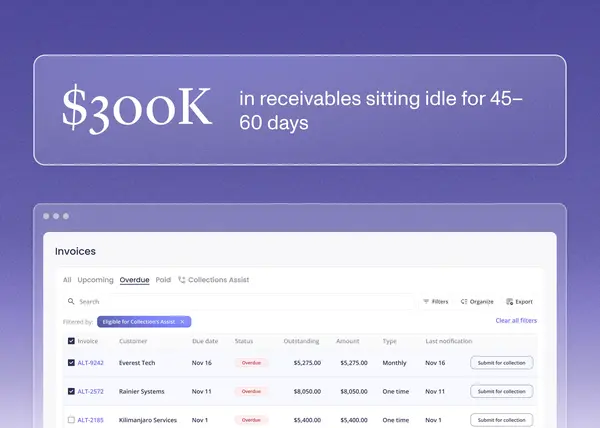

When I ran the numbers for another MSP, I saw something that made us both cringe: nearly $15,000 a year vanishing into credit card fees. We were in a Zoom room going through the P&L line by line when I spotted it—$14,892 in fees. The owner looked at me and said, “That’s a part-time intern for a semester.”

That’s not a rare case—it’s a quiet bleed happening across the industry. Not because MSPs are careless, but because they’re used to doing things the way they’ve always done them: checks in the mail, credit card payments over the phone, and a hodgepodge of workarounds in between.

It’s familiar. But it’s not sustainable.

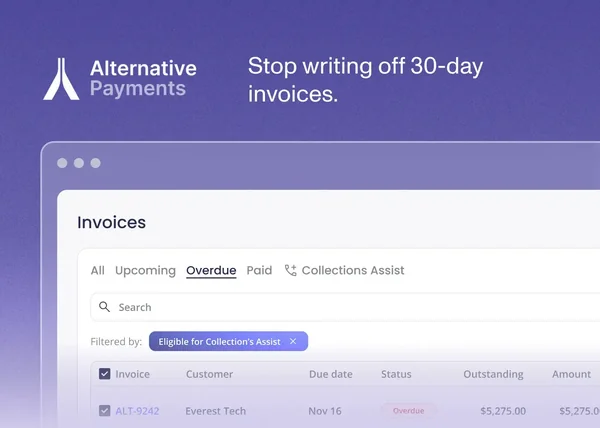

ACH—Automated Clearing House payments—often gets overlooked as the “boring” option. But for the modern MSP, it’s the workhorse that keeps margins healthier, operations smoother, and clients happier. The trick? Getting clients to make the switch.

Let’s walk through some of the big questions MSPs are asking—and along the way, we’ll uncover why one small change in how your clients pay can have a big impact on your margins, your operations, and your sanity.

The True Cost of Credit Card Payments

Credit card fees quietly erode profitability—and for many MSPs, the impact is bigger than they realize. Say you bring in $500K annually via credit card. With a conservative 2.5% fee, that’s $12,500 gone. If your gross margin is 20%, that means you’re keeping $100K in actual profit—so $12,500 in card fees is more than 12% of that. That’s over 12% of your bottom-line profit—directly impacting your EBITDA.

And that’s just the hard cost. Factor in:

- Manual reconciliation between your PSA and accounting system

- Time spent chasing down misapplied payments

- Payment errors, delays, and disputes

You’re paying with more than money. You’re paying with time—yours, or someone on your team’s. Probably both.

But here’s what many MSPs don’t realize: credit card fees scale in proportion to your success. As you grow, the problem compounds. Every new client you land who prefers to pay by card adds friction and cost to your backend. It’s like hiring more techs but giving them slower tools every time they close a ticket.

Plus, some merchant providers add additional charges like PCI compliance fees, monthly gateway fees, or batch processing charges. These hidden fees might not show up on your P&L as clearly—but they quietly chip away at your profitability. If you’re not already using the Service Leadership Index Chart of Accounts, this is a great moment to consider it. It gives you sharper, more actionable visibility into where your money’s going—and how to make it go further.

And there’s a psychological toll: cash flow unpredictability from chargebacks, delays in deposits, and admin fatigue trying to sort it all out. When your team spends time correcting billing issues or explaining late fees to frustrated clients, you’re losing out on productivity, morale, and reputation all at once.

So while card acceptance feels like convenience, it’s often a luxury MSPs are unknowingly paying for with their margins—and their sanity. But here’s the good news: there’s a smarter way to get paid that benefits both sides of the relationship.

Why ACH Is a Win-Win

According to Nacha, over 30 billion ACH payments were processed in 2023 alone, a testament to how embedded this payment method has become in the modern B2B economy. Leading platforms like Bill.com and Stripe actively encourage ACH usage for recurring billing models—not just for cost savings, but because it delivers predictability, reduces churn, and improves user experience.

ACH isn’t just convenient—it’s what mature, scalable businesses rely on.

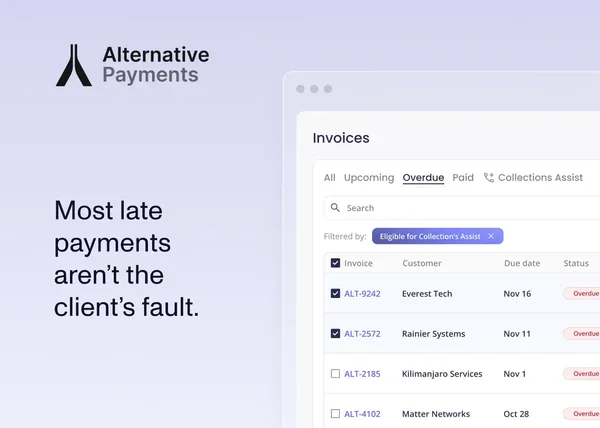

Here’s the part we don’t talk about enough: clients don’t want to be a pain. Most are open to options that simplify things—as long as it’s framed well. But education alone rarely changes behavior. What actually moves the needle is understanding what clients are afraid of, what motivates them, and how to reduce the friction of change. That’s where the psychology comes in.

For you (the MSP):

- ACH processing fees are dramatically lower (think pennies vs. percentages)—and with Alternative Payments, they’re free.

- Fewer errors and chargebacks. ACH payments don’t rely on expiring card details or manual re-entry, which reduces the likelihood of failed transactions. And unlike credit cards, ACH isn’t subject to the same kind of chargeback mechanisms, making reversals far less common.

- More predictable fees. Unlike interchange-based card processing, which can vary dramatically depending on the card type, ACH costs are flat and far easier to budget for.

For your clients:

- No check-writing, envelope-stuffing, or stamps.

- Set-it-and-forget-it autopay.

- Fewer late fees or accidental service interruptions.

- More professional experience.

When you explain it this way, ACH stops being a cost-saving maneuver and becomes a service upgrade—for everyone involved.

And yet—even with all of these advantages laid out clearly—some clients still hesitate. That’s where the real work begins.

Handling Common Objections (Without Losing the Client’s Trust)

Even when you’ve clearly communicated the benefits of ACH, clients may hesitate—and that’s normal. People are naturally cautious when it comes to changing how they pay. They’ve developed habits around credit cards or checks, and even small changes can trigger bigger concerns: “Is this secure? What if there’s a mistake? What’s in it for me?”

The good news is that most objections are both predictable and manageable. If you meet them with empathy instead of pressure, and pair reassurance with practical solutions, clients will often surprise you with their willingness to switch.

“ACH has a limited dispute window.”

That’s a feature, not a bug. Unlike credit cards, which can allow chargebacks for up to 120 days, ACH disputes are typically limited to around 60 days. That tighter window encourages clarity up front, reduces fraudulent reversals, and minimizes long-term cash flow surprises.

“But I get points on my credit card.”

Totally fair. But those rewards aren’t really free—they’re funded by the fees charged to the business. When clients pay by ACH, they help reduce overhead that could otherwise drive up service costs.

“Is ACH secure?”

Absolutely. ACH transactions are transmitted through tightly regulated, bank-to-bank networks and are encrypted end-to-end. Many clients don’t realize ACH is the same method used for payroll and IRS tax refunds.

The key is not to dismiss these concerns—but to use them as a bridge. When clients feel heard, they’re more likely to act. And once you’ve answered their questions and diffused their fears, you’ve earned the right to guide them toward the next step.

How to Encourage Clients to Switch

By now, you’ve tackled the concerns, answered the tough questions, and shown clients that switching to ACH isn’t a risk—it’s a smart, secure upgrade. So the next logical step is helping them take action. This is where subtle strategy and client-centered thinking come into play. Instead of pushing, guide them. Make ACH the easiest choice in the room—and watch how many say yes without a second thought.

Once you’ve addressed the concerns and cleared the air, it’s time to shift the conversation from why ACH makes sense to how to make it happen. This is where you lead with simplicity, not pressure. The key is to remove friction, create positive reinforcement, and let the transition feel like a favor—not a chore.

This is behavioral science more than finance. People resist change not because they’re stubborn—but because change feels like work. So we make it feel like less work.

- Make ACH the default. Position it as the recommended option in every invoice or payment screen.

- Offer small ACH incentives. A 1–2% discount for ACH payments (or a credit card surcharge) reframes the economics for your client.

- Keep setup simple. One link. One click. Done. Clients should never need to “figure it out.”

- Reinforce the value. A simple note on invoices or during onboarding: “Paying via ACH helps keep our costs (and your prices) down.”

And don’t underestimate the power of conversation. If a client is hesitant, ask them: “What’s holding you back from ACH?” You’ll learn more in that one sentence than in a dozen emails.

The Alternative Payments Way

Once you’ve addressed the concerns and cleared the air, it’s time to shift the conversation from why ACH makes sense to how to make it happen. Lead with simplicity, not pressure. The key is to remove friction, create positive reinforcement, and let the transition feel like a favor—not a chore.

- Make ACH the default.

- Offer small ACH incentives.

- Keep setup simple: one link, one click.

- Reinforce the value: “Paying via ACH helps keep our costs (and your prices) down.”

Have the conversation: “What’s holding you back from ACH?”

And then—listen. You’ll learn more in a few minutes of honest feedback than in a dozen email nudges. When a client tells you what’s really holding them back, you gain not just insight, but an invitation. That’s your cue to help them over the hump.

You don’t need to convert everyone at once. Start with the clients who trust you most. Ask them if they’d be willing to try ACH for a quarter. Offer to walk them through the setup, or better yet—do it with them in real time. Use that experience to refine your process and build a playbook.

Small experiments lead to repeatable wins. And those wins—when documented and shared—become momentum.

Once you’ve got a few ACH converts, don’t let that story stay hidden. Mention it in your onboarding process. Highlight it on your invoices. Reference it during quarterly reviews. Normalize it. Make it the cultural default.

And when clients realize it’s easier, faster, and more professional? They’ll wonder why they didn’t switch sooner.

Small Shifts, Big Results

By now, you’ve seen how the right payment process isn’t just about collecting money—it’s about building trust, efficiency, and sustainability into your MSP’s operations.

Encouraging ACH adoption isn’t about penny-pinching. It’s about transforming how your MSP operates—from scattered, manual billing cycles to clean, reliable, scalable revenue management. It’s about showing clients that you’re thinking not just about what’s easiest for you, but what’s ultimately best for them, too.

With ACH, you lower your costs, yes—but more importantly, you gain predictability, improve relationships, and get back valuable time that can be reinvested into growth. This isn’t just a finance decision. It’s a leadership decision.

Start small. Audit your client payment mix. Identify one or two clients who are good candidates to pilot ACH. Offer them a smooth, well-explained process. Listen to their feedback. Then repeat.

Every small improvement in your billing process ripples outward—to your team, your clients, and your bottom line.

And if you’re ready to accelerate the shift and simplify ACH adoption with the right tools—well, you know where to find us.

Not ready to switch tools yet? No pressure. If you’re curious how much you could save by moving clients to ACH, we’ll run the numbers with you—no pitch, no pressure. Just insight.

Simplify your customer payments, unlock instant cash flow

Keep reading