•

IT Services

•

Professional Services

•

Small Businesses

•

Security

November 28, 2025

Hidden Dangers with Using High-Risk Payment Processors

If you have ever opened your payment dashboard expecting money to land in your account and instead found nothing there, you already know how stressful IT payments can become when something goes wrong. Most MSP owners choose a processor based on speed, familiarity, or ease of setup. What they may not realize is that some processors categorize certain industries under higher-risk profiles, which can influence fees, reserves, and payout schedules. Entire industries are considered high risk, including reserve clauses that allow funds to be held for risk or compliance reviews and operate with payout windows that stretch far longer than what most MSPs can afford.

PaySafe is a great example because you can verify their reputation publicly. Many public Trustpilot reviews for PaySafe mention sudden holds, limited communication, and unpredictable payout timing.

When you are with a processor that treats you like a high-risk account, your access to your own money becomes unpredictable. You could hit a certain transaction amount, a certain volume threshold, or even just have a client with a large invoice come through, and suddenly your payout schedule stretches to several days. For MSPs juggling payroll, licenses, and vendor costs, even a three-day delay can disrupt cash flow. A seven-day hold can be disastrous.

This blog breaks down how high-risk processors create instability, why MSPs are uniquely vulnerable, and what you can do to protect your business before a payout delay catches you off guard.

How High-Risk Processors Quietly Label Your Business Without Telling You

One of the most frustrating parts about working with a high-risk processor is that they rarely tell you that you have been classified this way. You simply discover it when something goes wrong. High-risk processors use internal scoring rules that are not visible to you. Businesses may be flagged under higher-risk categories because certain transaction patterns or service models align with broader industry risk criteria, such as industry type, invoice size, or client spending patterns, or even random algorithmic triggers.

The problem is that MSPs often do not belong in these high-risk categories at all. You are running a recurring revenue business with predictable billing, not running an online casino or a sketchy subscription box service. But some high-risk processors group together a wide range of industries based on internal risk models the merchant cannot see.

This matters because once your account is flagged, every payout becomes uncertain. Your volume might look too high this month. A single large invoice might trigger a manual review. A spike in transactions might send you into an eight-day payout window. And you will not know when it is coming.

The Psychology of Payment Fear: Why Uncertainty Around Payouts Damages Your Business

Let’s be honest here. Money delays feel personal. When your payout does not arrive on time, it does not matter whether the issue is technical or procedural, it hits you emotionally first. It feels like something is wrong, even if you cannot see it yet. And when your cash flow is tied to payroll, software renewals, and vendor services, uncertainty becomes stressful fast.

MSPs typically operate with tight operational rhythms. Tools must be paid for. Engineers expect timely paychecks. Clients expect uninterrupted services. When payouts stretch from one day to five or seven due to review or risk policies, the fear is not just losing money, it is losing stability. And financial instability, even temporary, affects how you make decisions, how you price services, and even how you feel about your business.

The Better Business Bureau contains publicly accessible merchant complaints related to payout delays or fund holds. Across these complaints, many business owners describe similar concerns about unpredictable payout timing.

For MSPs, that uncertainty is what creates fear. When payout schedules fluctuate without clear visibility, it can leave business owners feeling like they have limited control over when their money arrives, and that’s a difficult environment to run a recurring-revenue business in.

That is the real psychological danger. Unpredictable payout timing can push business owners into a defensive mindset, constantly waiting, refreshing the dashboard, and hoping this payout arrives on time. No MSP owner should run their business with that level of uncertainty.

Understanding Reserve Holds: How Processors Freeze Your Money Without Warning

Reserve holds are one of the most feared parts of payment processing, mostly because they feel like someone else is suddenly in control of your business’s oxygen supply. A reserve hold happens when your processor decides to keep a portion of your funds “just in case” there is a future chargeback or risk event. The challenge is that reserve decisions are guided by internal risk criteria, and merchants often only learn about a reserve after it has been applied.

PaySafe’s own legal terms confirm that reserve holds can be placed at the processor’s discretion for reasons such as security, compliance, or risk management. They state clearly that funds can be held or payout schedules changed when deemed necessary. These terms generally do not specify detailed triggers or clear thresholds for when reserves may be applied.

This means an MSP can process payments smoothly for months, then suddenly get flagged because one invoice came in higher than usual or a client disputed a charge. You might not even know the hold is coming until you notice your payout looks short or does not arrive.

In many cases, reserve decisions are driven by the processor’s internal risk scoring systems, not by any specific action taken by the MSP. Their internal scoring, their algorithms, and their manual reviews dictate whether you get tomorrow’s payout or next week’s payout. That kind of unpredictability is dangerous for a business that relies on recurring monthly cash flow.

The Payout Delay Trap, The Real Cost of Waiting Days For Your Own Money

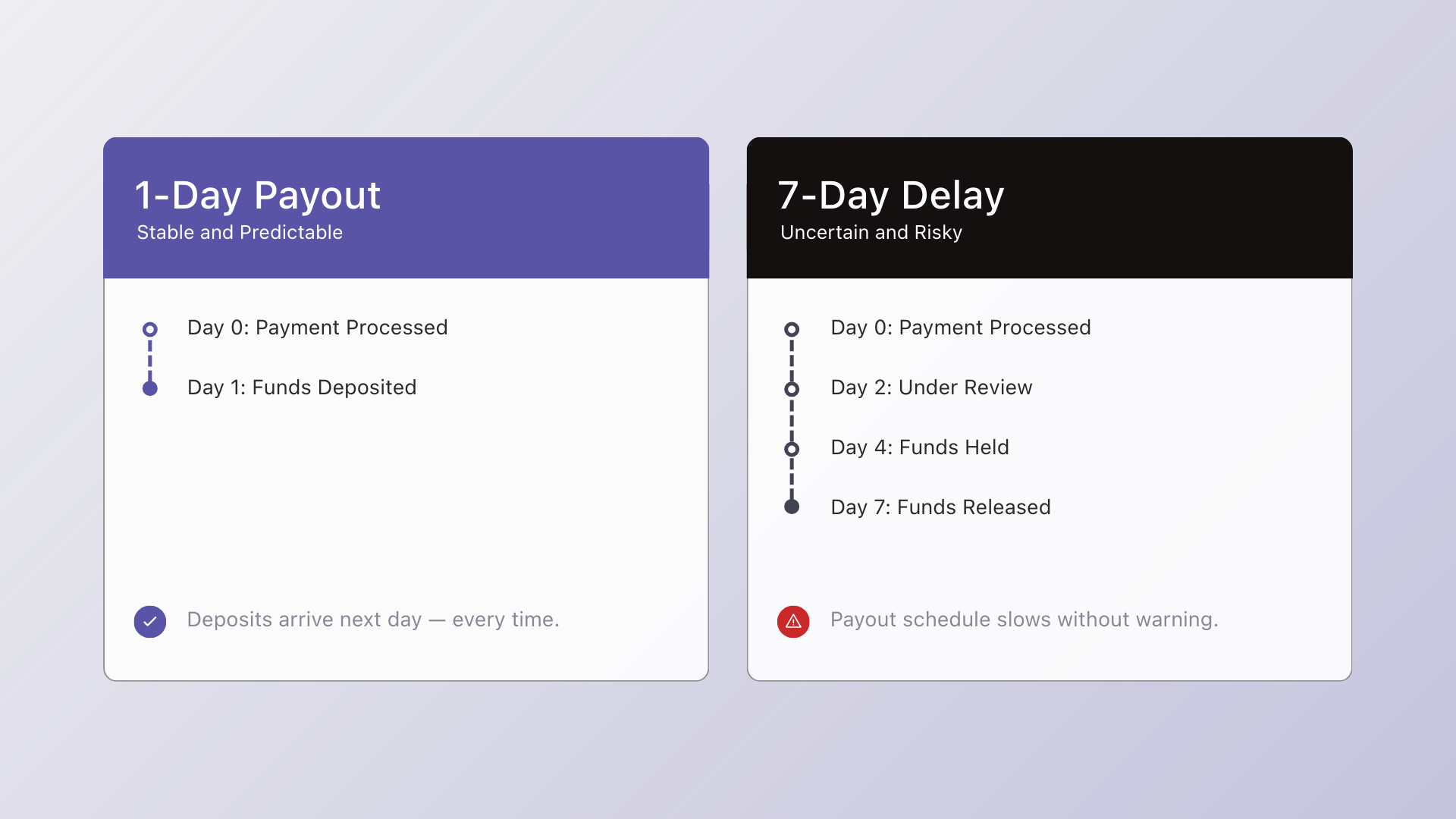

One of the biggest shocks MSPs experience after signing with a high-risk processor is how quickly payout timing can change. Maybe your first few deposits arrive the next day, and everything feels normal. Then one afternoon, you log into your dashboard and see that your next payout will now arrive in three days, or five days, or a full week. You did not change anything. Your business did not suddenly become risky. It may feel like your payout schedule has suddenly shifted to a slower timeline without prior notice.

These delays are not just frustrating. They disrupt payroll, vendor payment, and operational planning. MSPs are subscription-based businesses that rely on steady, predictable cash flow. Waiting six or seven days for a payout that used to take one day forces you to hold extra cash in your account. It makes planning harder and increases financial stress for absolutely no reason other than the processor decided to slow things down.

Some business owners on Trustpilot describe experiences where payouts were suddenly pushed to a multi-day schedule with little explanation.

When a processor can change your payout timeline on a whim, you lose control of your cash flow. And when you lose control of your cash flow, you lose stability. Every MSP owner knows that stability is the backbone of monthly recurring revenue.

The Difference Between Normal IT Payments and High-Risk Ones

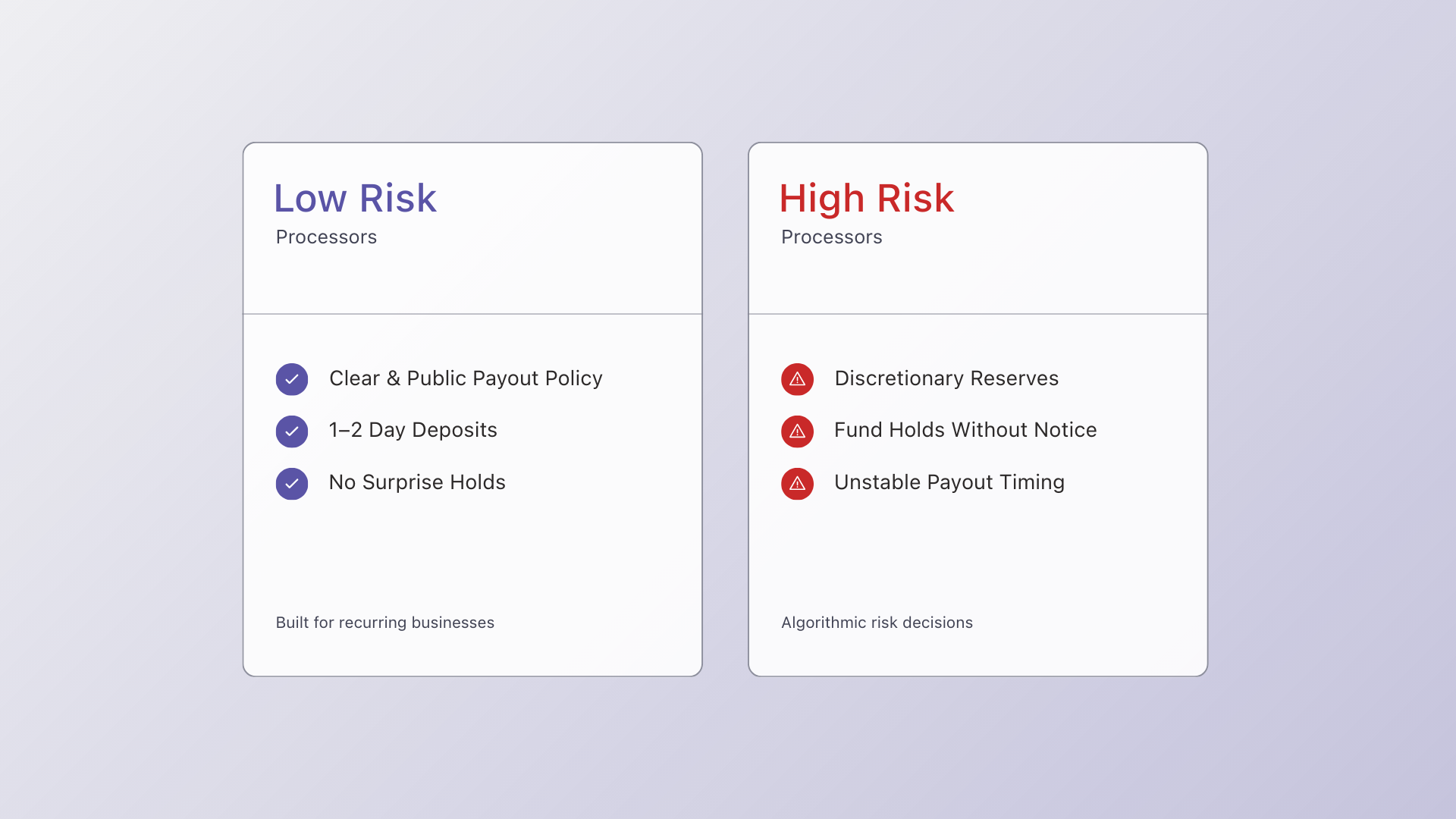

Most MSPs are surprised to learn that they almost always qualify for mainstream payment processors with stable payout schedules and transparent rules. Companies like Stripe, Square, and Adyen all publicly document their payout timelines and reserve policies. They are built for businesses that want clarity.

Stripe, for example, lists its standard payout schedule by country in a well-organized, public page.

Square also explains exactly when to expect deposits, and its help center breaks down timing for each account type.

Adyen provides transparent documentation for its payout process as well. Their issuing payouts documentation outlines how and when funds are released.

Compare that to a high-risk processor that simply says payouts may vary or that reserves may be held at their discretion. Many MSPs qualify for mainstream processors with transparent payout schedules. With high-risk processors, you often find out the rules only after your money is already being held.

For MSPs that rely heavily on recurring billing, transparency is not a luxury. It is a requirement. You need to know exactly when money lands in your account because it determines everything from payroll to software renewals.

How to Know if Your Processor is High-Risk: Simple Checks You Can Run Today

You can usually tell if your processor is treating you like a high-risk merchant by looking closely at a few areas. The first place to look is your payout schedule. If it is inconsistent, changing frequently, or slower than what industry-standard processors offer, that is a red flag.

Another indicator is whether the processor mentions reserves in your agreement. High-risk processors almost always include language that lets them hold your funds for risk management. They do not always tell you when they will use that clause, but they reserve the right to do it whenever they feel it is necessary.

Merchant Maverick provides an excellent guide that helps businesses understand what a legitimate merchant account looks like and what warning signs to watch out for. It is a great reference if you want to compare the stability of your current processor to industry expectations.

If your processor has a high volume of public complaints about frozen funds, delayed payouts, or poor communication, that is another clear sign. When a large number of business owners report similar issues, the processor is not unlucky. It is operating with high-risk policies.

How MSPs Can Vet a Processor Before Trusting Them with Cash Flow

Before you choose a processor to manage your revenue, it helps to think of the decision the same way you think about evaluating a new vendor for cybersecurity. You would never trust a vendor that would not explain how they protect data. The same logic applies here. It’s a red flag if a processor cannot clearly explain how and when they release funds.

Start by reading the payout schedule line by line. If the processor says payouts are released in one to two days, but then follows that with language that allows them to extend payout times for risk, that is a clue that delays might happen later.

Next, look at how they handle reserves. If reserves can be placed at the processor’s discretion, that means you have no guarantee of access to your funds if they change your risk score.

Communication is another important factor. The Federal Trade Commission has a public guide that helps small businesses understand payment processor terms and what red flags to avoid. It is a great resource for understanding how to evaluate the fine print.

Lastly, test their customer support. If you cannot get a real person on the phone before becoming a customer, you are unlikely to get one once they are holding your money.

Processors that are transparent, responsive, and predictable tend to be low risk. Processors that hide behind vague policies or inconsistent service tend to cause financial trouble.

Dependable IT Payments Are a Retention Tool, Not Just a Billing Choice

Payment processors are not all created equal. Some give you clarity and peace of mind. Others introduce instability that affects your cash flow, your planning, and your confidence. When processing terms determine payout timing and fund availability, your cash flow becomes unpredictable—and that uncertainty can disrupt normal business operations.

Stable and transparent IT payments are more than a convenience. They are a retention tool. Your clients stay with you because you feel dependable. It is hard to project dependability when payout timing feels inconsistent or unclear.

You do not need to overhaul everything at once. Start by reviewing your current processor. Check your payout timing. Look at your reserve language. Research public reviews. And make sure your processor deserves the level of trust you are giving it.

The more stable your payment system becomes, the more stable your business feels. And that kind of stability is what keeps MSPs growing year after year.

Simplify your customer payments, unlock instant cash flow

Keep reading

How MSPs Automate Payment Processing and PSA Reconciliation

AP Software That Shows What's Outstanding and Paid: A Practical Guide